“YOU’RE ALWAYS ON MY MIND…….YOU’RE ALWAYS ON MY MIND……”

Willie Nelson, Singer/Song writer

Inflation is on everyone’s mind, all the time. There is no economic indicator which carries as much import today– because it is the focus of every central banker and every parent who walks down a shopping aisle. So, let’s catch up with inflation to see where it might be going, not where it has been.

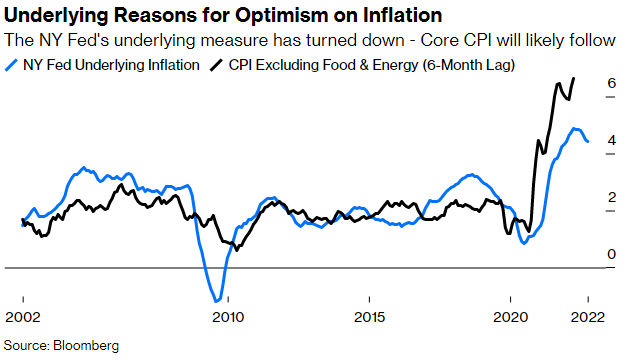

The New York Federal Reserve has for some time used some complicated math to calculate an underlying rate of inflation. Included in this math are prices in the CPI as well as other macro variables. As seen below, the CPI has tended to follow the New York Fed’s model by several months – but follow it, it does. Already the Fed’s underlying rate has fallen and in fact the delta between the two curves (2.2%) is as large as it was in September 2009. After reaching that spread in 2009, the core CPI collapsed.

CHART 1

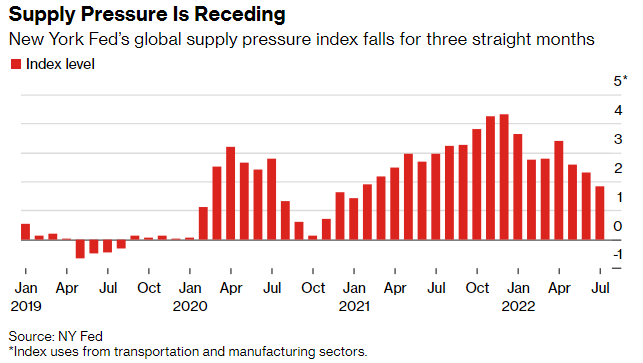

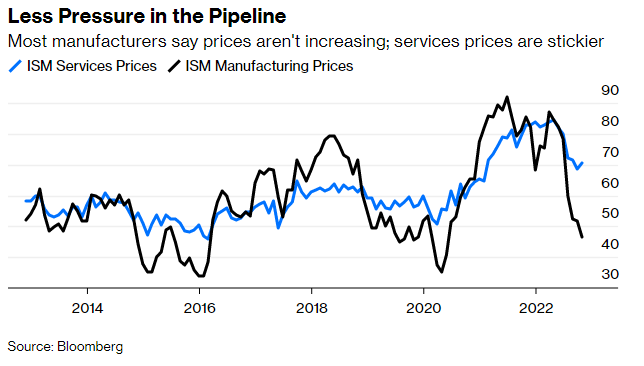

Supply chain disruptions, which have been a major source of inflation for months, have been getting “de – bottlenecked.” Below is the New York Fed’s global supply chain pressure index (Chart 2). Please note that it has fallen for months, alleviating cost pressures throughout manufacturing which can also be seen in a very pronounced fashion in Chart 3 when one looks at the ISM Manufacturing Prices Index.

CHART 2

CHART 3

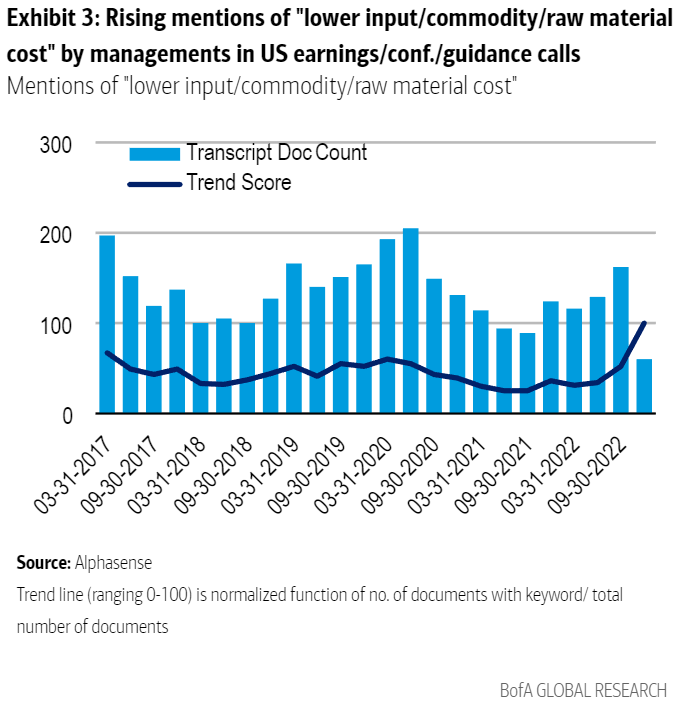

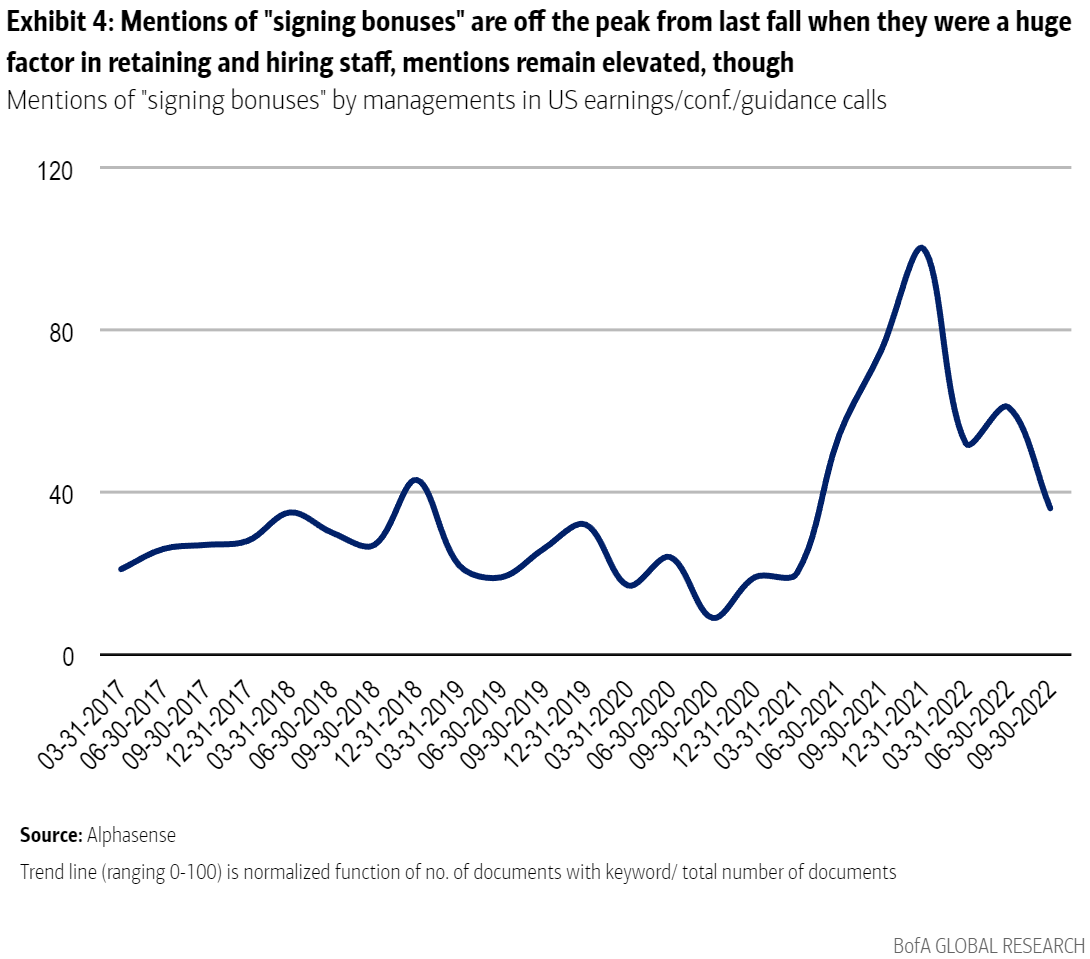

Further, corporate CEO’s and CFO’s are talking more on quarterly earnings conference calls with Wall Street analysts about lower input prices (i.e., lower commodity prices) for their manufactured products.

CHART 4

CHART 5

None of the aforementioned is absolutely conclusive of peak inflation. But it is very suggestive. If inflation is determined by the Fed to be a problem that is or nearly well in hand, then perhaps interest rates would not need to rise too much more. Then perhaps if the U.S. faces a recession, it would not be too severe. Then perhaps consumer/investor sentiment would change for the positive. Then perhaps the stock market would find its footing and the Price/Earnings multiple compression that investors have suffered with so far in 2022 would reverse with lower interest rates, brighter corporate earnings outlooks and higher equity and bond prices. Just perhaps….