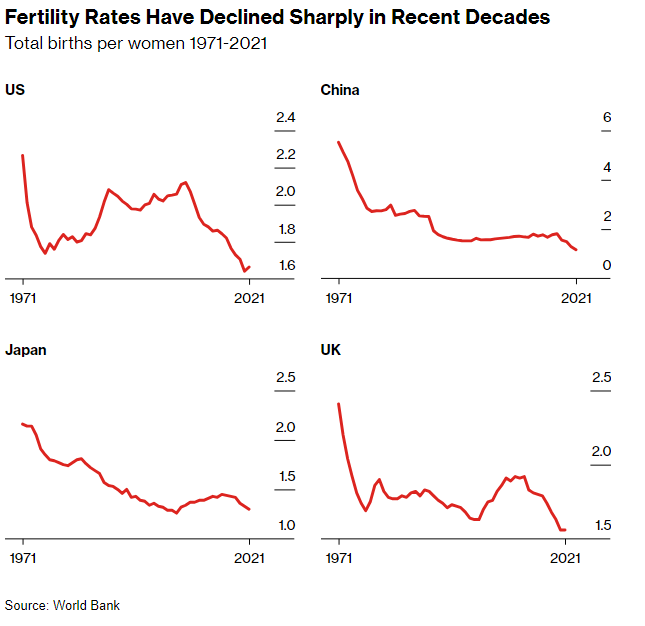

As a world, we are not getting any younger. This unfortunately is because fertility rates declined sharply from 1971 – 2021 as can be seen in the following chart:

CHART 1

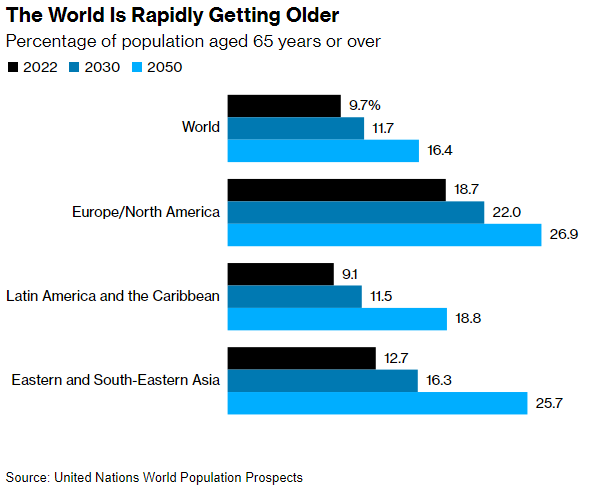

There are some countries where the young have held their own as a percent of population (think India) – but by and large, the world is getting older.

CHART 2

This will mean that some time in the future, not too distantly either, there will be fewer workers to carry the social benefits’ burdens for the more numerous living retirees. Enhanced worker productivity (think AI) and immigration can help stave off the inflationary effects on an economy growing less productive due to a larger elderly population. But they may not be enough of an economic counterbalance to win the day. So, what might an investor do?

Traditionally it has been prudent practice to weight an investor’s portfolio more heavily with bonds as the investor aged. The rationale has been that when an investor is young, he/she can accept more account volatility because there is more time to recover any paper losses. As one ages, there is obviously less time for portfolio recovery after a bad stock market episode. But if the demographics charted above hold true, there might be a bit more inflation than most people have experienced for years. Please remember that for most of the 2010’s the US, along with other countries, was fighting disinflation – i.e., inflation rates that were sometimes slightly negative. With fewer future workers, employers will have to bid up wages to attract employees. The Fed is now targeting a 2% inflation rate. Inflation has never been good for bonds and never will be because it erodes the value of fixed income over time. Bonds do not grow like stocks. If the demographic future outlined above comes true, then perhaps a higher allocation to equity (US and international), commodities (real or as represented by certain equities) and infrastructure projects (again real or as represented by specific stocks) might be a better way to fight inflation, because equities can grow in spite of and faster than inflation.

We are not eschewing all fixed income for a portfolio. We are simply suggesting that if you believe that inflation may be more significant in the future than it was in the past, then perhaps the weighting of bonds in one’s portfolio should be less than it was traditionally.

May 31, 2024

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research and Chairman of the Board for the Independence Seaport Museum. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.