According to the Social Security Administration’s January 2024 publication of “Understanding the Benefits”, Social Security affects almost every family in the United States of America. The goal for Social Security is to be able to replace a portion of income for people who retire, people who develop disabilities that affect their ability to work, and families in which a parent/spouse has died. Of those three major categories, retirement is the only area where individuals have a choice of timing.

The system for Social Security retirement benefits is set up to allow you to elect to start taking those benefits as early as age 62, but there are several factors that could make it more advantageous to wait until age 70 to start taking benefits.

To help make the decision of when to start taking benefits, you can sift through these factors and their implications by answering the following questions:

1. Are you eligible for Social Security?

To be eligible for Social Security, you need to earn Social Security credits. A taxpayer can earn up to 4 credits in a year for every $1,730 (2024 value) of reported earned income. To be fully insured for retirement benefits, a person needs 40 credits, or a minimum of 10 years of work.

2. Does the Social Security Administration have an accurate record of your earnings?

The amount of retirement benefits for which a person is eligible is based on their highest 35 years of earnings. Any year with no earnings counts as a $0 for benefit calculations. If there was a period when you did not work, such as taking an unpaid sabbatical or maternity/paternity leave, delaying taking Social Security may increase your overall benefit amount. You should create an account on the SSA.Gov website and check their record of your earnings at least once a year.

3. What level of income do you want and need to support your lifestyle as a retiree?

Social Security benefits are not, nor are they meant to be, a full replacement for the income made when working full time. All taxpaying citizens contribute to the Social Security funding, but you do not receive the same amount that you contribute. The income replacement value of Social Security benefits can range from 25% – 78% of pre-retirement income, but the higher your pre-retirement income, the lower your value of income replacement. When making this decision, it is most important to have a goal for how much cash your desired lifestyle requires. The longer you wait before taking benefits, the higher the monthly benefit will be.

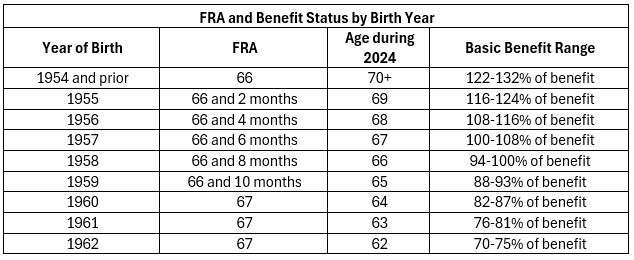

4. When were you born and what is your Full Retirement Age?

You are eligible to receive your full Social Security benefit at your Full Retirement Age (FRA). If you decide to take benefits prior to FRA, your benefits will be reduced by 0.5% for every month you start to take benefits prior to reaching FRA. If your FRA is 67 and you decide to take benefits at 62, you will only get 70% (60 Months * 0.5% reduction) of your full benefit. If you delay receiving benefits past FRA, your benefits will increase every month, up to age 70.

If you continue to earn income after starting to take benefits, your benefits will be reduced based on earnings limits and your full retirement age. See the included information tables to assist in determining FRA and the effects on your benefits.

5. What is your life expectancy?

Social Security benefits are paid out monthly, so therefore staying healthy, physically and mentally, is key to getting the most out of your benefits. If your life expectancy is on the lower side, you may want to start collecting earlier, to have cash available to fund your lifestyle. If your life expectancy is on the higher side, you may want to delay collecting benefits as long as possible, to maximize the effectiveness of the benefits in supporting your retirement.

6. Do you mind paying taxes on your benefits?

There are thresholds for earned income that could cause a portion of Social Security benefits to be taxable. For an individual taxpayer, this threshold is $25,000 and $32,000 for joint filers. If you have earned income above this amount, up to 85% of your received Social Security benefits may be taxable. If you have a full- or part-time job while collecting Social Security benefits, you should be prepared to pay taxes and have them withheld from your monthly distributions.

7. Did you get divorced?

If you are divorced, having been married for at least 10 years, currently unmarried, and at least 62 years old, you may be eligible to collect benefits from your ex-spouse’s account. If they have not started collecting benefits yet, you need to be divorced for at least 2 years. If you are at least 60, or at least 50 with a qualifying disability, and your ex-spouse dies, you may also be eligible for survivor benefits from their account. You need to be eligible for less benefits than your ex-spouse, and in this scenario, Social Security will increase your benefit to match those of your ex-spouse.

8. Did someone in your family pass away after earning enough Social Security credits?

There are Survivor benefits as part of the Social Security program for family members. A surviving person aged 60 or older or at least aged 50 with a qualifying disability can receive benefits from their late spouse’s account. A surviving person of any age taking care of a qualifying child can receive benefits from their late spouse’s account. A surviving child meeting the following requirements can receive benefits from their late parent’s account: unmarried, younger than 18, between 18 and 19 enrolled as full-time students, or 18 and older with a qualifying disability. Dependent surviving parents can also receive benefits. In most cases, you can file to start collecting benefits online, but for Survivor benefits, you must call the Social Security Administration or go to one of their offices to work with a Social Security representative.

Social Security is part of most American’s retirement plans. These questions just touch on the factors that go into the best strategy for funding your retirement lifestyle. Working with a financial planner and team, like we have available at Baldwin Management, is the best way to develop a comprehensive strategy to live the way you want to in retirement. If you are interested in taking advantage of our services, please contact our Family Office team at (610)260-1555.

Benjamin Meck, CPA,

Tax/Accounting Associate

Benjamin joined Baldwin Family Office in 2023 after spending 8 years gaining experience in corporate, cost, construction, and property accounting.

He holds a B.S.B.A in both Accounting and Finance from Bloomsburg University of Pennsylvania. He earned the CPA designation in 2022. He is a member of the Pennsylvania Institute of Certified Public Accountants and the National Association of Tax Professionals.