I CAN’T GET A JOB………

Despite record low unemployment rates, there are many 2023 graduates still seeking jobs. Companies like Amazon, Meta, Alphabet, Goldman Sachs, Morgan Stanley – once much sought after places to land an offer – have chilled a bit. Hiring has slowed and firings have risen. In 2022, advertisements for entry level jobs were 80% higher than in 2019, according to Revelio Labs, a workforce intelligence firm. By May 2023, entry level openings were only 3.7% above 2019 levels. Demand for experienced workers has stayed strong, as in many cases, the experienced worker has decided to take on some entry level tasks. We wonder if this could be reflective of job uncertainty creeping into the workplace? Further, we wonder if there won’t be some spillover effects on wage inflation? We think the answer to both will be yes.

CHINA BLUES…….

To date, 2023 has not been a good year for the Middle Kingdom. Expected to leap into the New Year with Covid restrictions lifted, the unbound economy has performed not much better than a damp squib. Youth unemployment is at record levels (>21%). The real estate industry (25% of Chinese GDP) is on its back foot. Country Garden, now the largest mainland residential developer, is worryingly close to collapse. Evergrande, formerly the largest Chinese developer, recently emerged from some lender protections, went public again and had its stock dive 80% on the first day of trading. Tech companies (think Alibaba, Tencent, Baidu) which were once darlings of the government have won some reprieves. Operations are ramping up – but restraint is probably a watchword for management teams, so as not to irritate state bureaucrats who have ultimate authority. With each succeeding reporting period, economic news from China has not improved, nor is it expected to in the near future. The government is fighting disinflation, if not deflation. Already, various economic tools are being implemented to “gin up” China’s economy. Hidden debt at local government levels, where most borrowing occurs, is disturbingly high. The central government has a mighty task before it if it is to successfully energize the economy. The renminbi is falling and China, the world’s second largest economy, is exporting disinflation through its currency and through its efforts to stimulate economic growth by cutting prices for goods and services. The U.S. is a large trading partner of China’s, despite all the conflicts between the two nations. So while China is economically suffering a bit right now, the U.S. should benefit with lower Chinese prices dampening inflation embers here at home.

UNLOVED – BUT CHEAP….

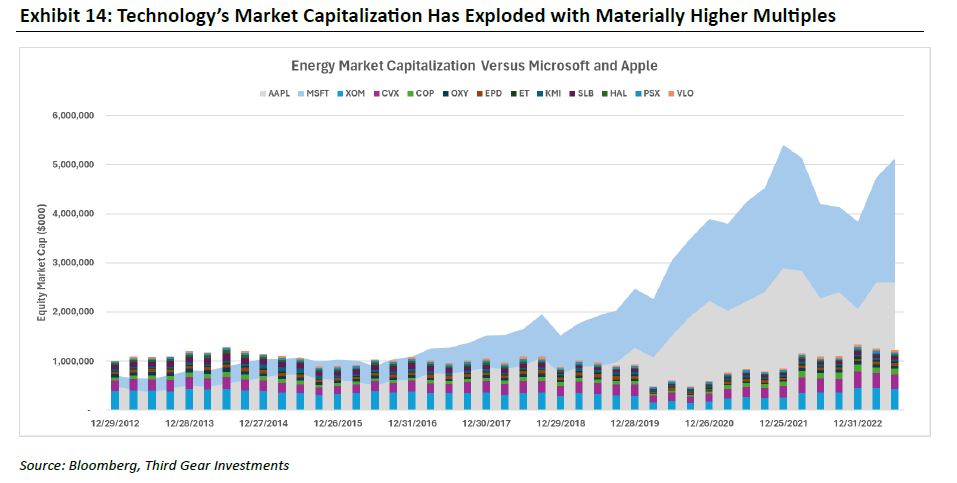

Hydrocarbon companies (think oil & gas, mid-stream pipeline operators) are largely without friends in the capital markets. When once these companies used to have a weighting of 15% in the S&P 500 (Sept. 1990) they now have a 4% weighting. There are a host of reasons why – including environmental arguments, poor capital allocation by management teams, etc. – with the result being that investors have pulled a lot of money out of such investments, and they have become very cheap. Following is a rather startling chart which compares the market capitalizations of some of the largest energy corporations (including Exxon, Chevron, Enterprise Products, Haliburton and SLB) to the capitalizations of Apple and Microsoft.

CHART 1

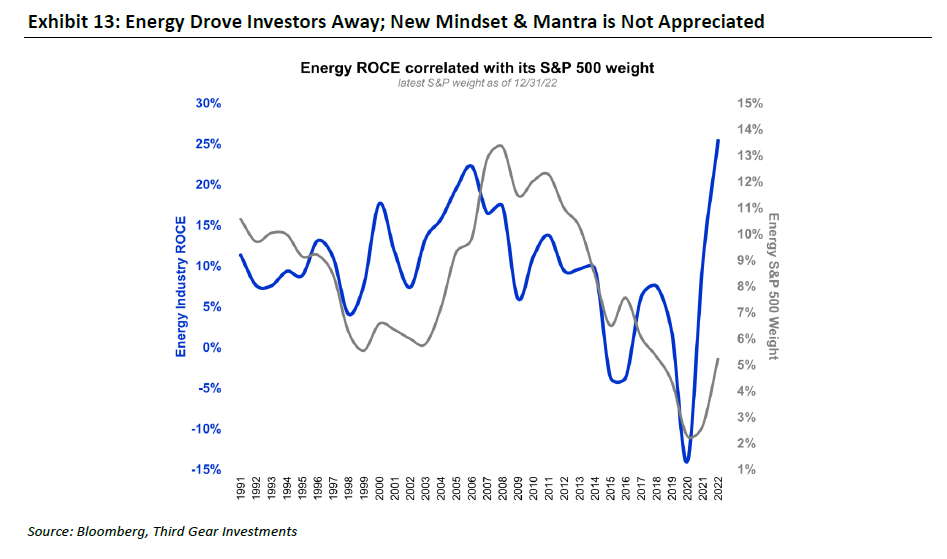

It is a shocking picture to see that Apple and Microsoft have larger market capitalizations than several huge energy companies – even ExxonMobil. In the next chart, we look at the correlation between energy return on capital employed (a marker of profitability) and the energy weighting within the S&P 500.

CHART 2

The above would strongly suggest that because of the energy industry’s strong rebound in profitability, energy stocks should rise and reclaim a larger share of the S&P 500’s weighting. No matter what one’s philosophical leaning is with regard to global warming, we contend that the world will not convert to an all-electric energy model anytime soon. It will be decades before most of the world’s energy needs are supplied by sources other than hydrocarbons. For some current uses of hydrocarbons there are no reasonable alternatives. We think that an energy mosaic will emerge – with a mix of energy sources like wind, solar, hydro, hydrogen, oil, natural gas, geothermal, propane, butane, etc. to power the world. Currently, old line energy stocks are being priced like they are the last of the dinosaurs. We think there could be some opportunity.

HAVE A GREAT LABOR DAY!!!