In fact, a lot of people are in a mood and it’s a pretty foul mood. Understandably so, we would say, for there are quite a few things which are unnerving – the war in Ukraine, inflation, rising interest rates, supply chain worries, and a rolling China shutdown of manufacturing are the ones grabbing headlines. These are the issues in the front of many minds and which have affected investor sentiment.

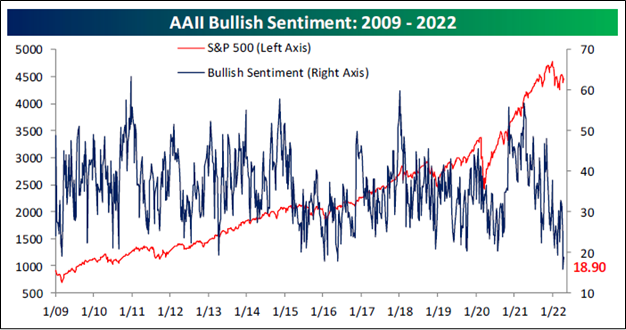

CHART 1

Source: The Bespoke Report 4/22/22

Above the reader will note a chart which overlays performance of the S&P 500 on the AAII (American Association of Individual Investors) Bullish Sentiment Index. Currently, with a reading of just 18.90%, the index is registering extreme bearishness. For perspective, a reading below 20% is rarely seen. But if one closely looks at the chart, it has been at times like now – when investors are fretful and investors have sold – that historically forward stock performance has been very rewarding. Who doesn’t like a bargain? Shouldn’t you buy when everyone thinks equities are going down? After many investors have sold, they can’t sell any more; they can only buy. This is why this investor sentiment index has proven to be such a powerful contra indicator of stock performance over the years.

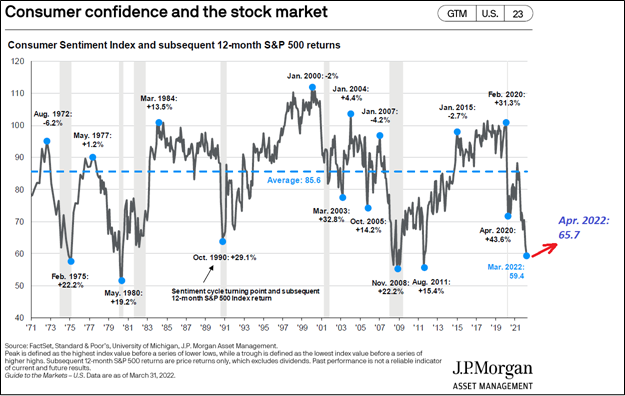

Following is another interesting chart – one that compares consumer confidence to stock market performance.

CHART 2

Source: JPM Guide to the Markets – U.S.

We have written in the past about the importance of the American consumer to the US economy. Approximately 70% of the American economy is driven by the consumer. So, if the consumer is feeling good or better, then the economy moves ahead. As you will see in Chart 2, when there has been a sentiment cycle turning point, especially when the cycle has turned positive, then the S&P 500 has performed very well in the subsequent 12 months. The April reading for the University of Michigan’s Consumer Confidence Index was 65.7, up from March’s reading of 59.4. While the worries noted above are certainly extant, perhaps counterbalancing considerations like strong jobs markets, higher incomes, lower Covid infections, effective Covid therapeutics and the coming of spring have cheered people. Whatever the cause for the turn in consumer psychology, it is, more often than not, a fact that the U.S. economy does not go into recession if the American consumer is feeling increasingly positive about their circumstances. Further, the stock market also seems to do well after consumer confidence troughs.

Who knows when there will be a positive investor mood swing? When that change becomes apparent, the markets, we think, will “roar off”. When the Ukraine war settles down, when inflation numbers begin to fall after the series begins to annualize and thus strips out early low numbers, when supply chains are again more functional, when Covid is no longer feared but simply managed – then we think investor moods will brighten. While we cannot time the improvement in any of these problems, we do know they are each being worked on intensively and we are probably closer to their resolutions than their beginnings.