Many investors are advised to build an “income portfolio” as they transition into retirement. For those who have seen their investments grow over a lifetime, it may be possible to fund their future living expenses from portfolio income alone, allowing for the income producing investments to create a legacy through inheritance. This can be great advice for those with enough wealth to put this plan into action. However, not all portfolio income is the same in the eyes of taxing authorities. This piece will examine the different types of portfolio income and their respective tax treatments.

Dividends (Qualified vs. Ordinary Dividends)

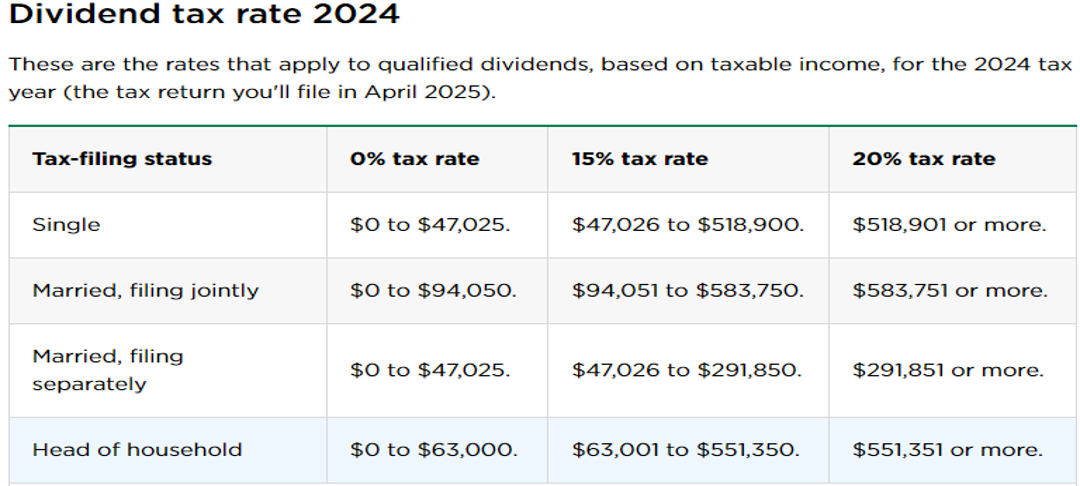

Prior to 2003, all dividends were taxed at the taxpayer’s normal income tax rate. That year, the tax law was changed to create the “qualified” dividend. This allowed for a lower tax rate on stock dividends, equal to the long-term capital gains tax rate, provided that the stock had been held for at least 60 days. For most investors, particularly high earners, these qualified dividends are an extremely attractive form of portfolio income as the federal tax on these dividends is capped at 20%.

Note: The tax rates shown below do not include your state’s income tax (if any) and the 3.8% Net Investment Income Tax (NIIT) for high earners.

Source: Nerdwallet

Ordinary dividends, also known as non-qualified dividends, do not receive the preferential tax rates shown above. Rather, they are taxed as ordinary income at the same marginal tax rate assigned to wages, bonuses, tips, commissions, etc. For high earners, the difference in taxation versus a qualified dividend is significant. Examples of investment vehicles that may pay ordinary dividends are Real Estate Investment Trusts (REITs) and some foreign stocks.

Note: One can place a REIT investment within a retirement account rather than a taxable account to avoid being subject to the higher tax rate on its dividend payments.

Bond Interest (Municipal, Government, and Corporate)

Municipal Bonds are those issued by states, cities, and counties. These are known as “tax-free municipals” and are exempt from federal income tax. If you live in the municipality in which the bond was issued, then there is no taxation at that level. For example, a Pennsylvania resident invests in a Pennsylvania Turnpike bond – he or she will not pay federal or state income tax on the bond’s interest payment. This is an attractive form of income for high earners, particularly those living in states with onerous state income tax rates.

Notes: Tax-free municipals should not be owned in retirement accounts. Taxable municipal bonds do exist, generally offering higher yields without the tax benefits of a tax-free municipal bond.

Government Bonds are debt instruments issued by the U.S. Department of the Treasury used to fund the government. These are often referred to as T-Bills or Treasuries. These bonds are backed by the full faith and credit of the U.S. Government and are among the safest investments in the world. In exchange for this safety, investors usually accept a slightly lower yield. Their terms to maturity range from three months to thirty years. From a tax standpoint, government bond interest is taxed at the federal level as ordinary income but is exempt from state taxation.

Note: A common misconception is that government bonds are exempt from federal taxation because they are issue by the government. This is not the case. They are exempt from state tax only.

Corporate Bonds are the debt of individual companies. These bonds often offer higher yields for investors to compensate for the additional risk of default as compared to a municipal or government bond. These bonds are attractive to investors looking for a higher return from their bond portfolio. Generally, a corporate bond’s yield is correlated with the financial stability of the issuing company. Investors will require a higher yield to be compensated for more risk and vice versa. These bonds are the least tax friendly, as their interest payments are taxed as ordinary income at both the federal and state levels.

Note: For investors with multiple account types, placing a higher yielding corporate bond in a retirement account is a tax efficient way to invest.

CDs, Savings Accounts, Money Market Funds

Income from these investment vehicles is treated as ordinary income. They are taxable at the federal and state tax levels and do not offer any beneficial tax treatment compared to other income sources.

Note: Some banks and brokerages offer tax-free Money Market Funds. Unless identified as such, assume that this interest is taxed as ordinary income.

Rental Property Income

For those owning real estate, rental income is a common type of income used to supplement retirement needs. This income is taxed as ordinary income. A key advantage of this income type is that property owners may deduct insurance costs, mortgage interest, maintenance costs, and depreciation.

Note: This can be an attractive form of retirement income that offers diversification away from stock and bond market volatility.

Option Income (selling covered calls, puts, and other derivatives)

Income derived from selling options is always considered a short-term capital gain and is treated as ordinary income.

Note: This can be an effective way to generate additional income from stocks. However, it can involve some additional risk and complexity.

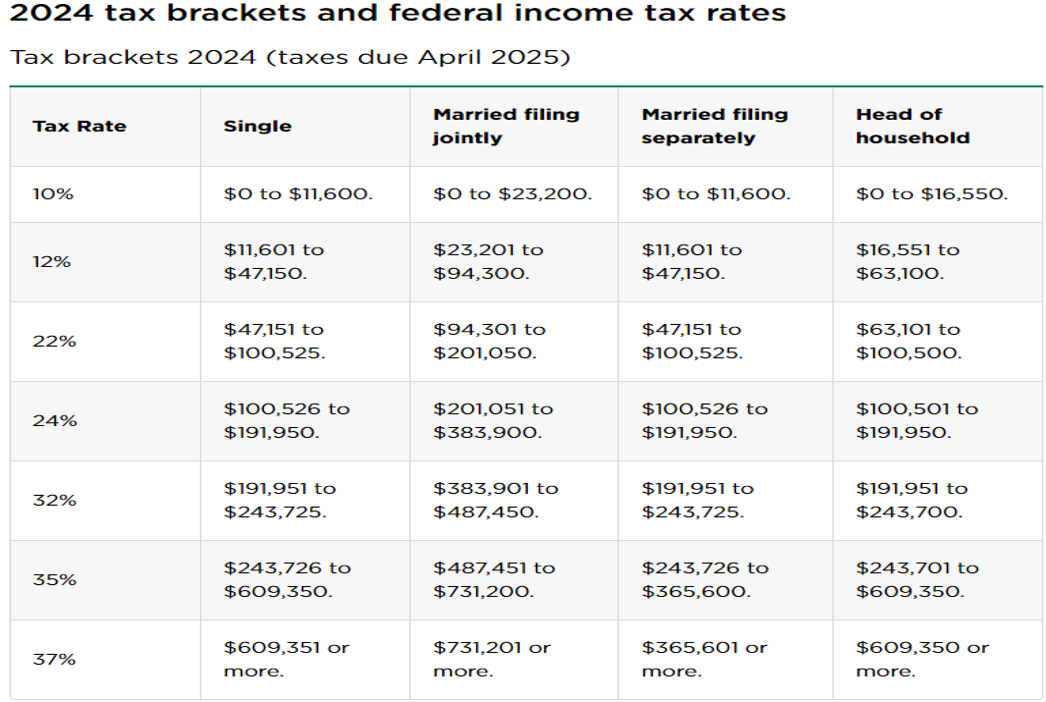

The table below shows the 2024 federal income tax brackets. This applies to the various sources of ordinary income previously described.

Source: Nerdwallet

If you currently have an income portfolio (or would like to build one) and are interested in an analysis of your holdings, please let us know. Your portfolio manager will work with Baldwin’s tax team to offer suggestions about which type of income producing investment is best suited for you. We can also advise on whether your income producing investments are optimally placed within your account types.

—- // —-

Sources: https://www.nerdwallet.com/, https://www.irs.gov, https://www.revenue.pa.gov

Baldwin Management LLC. (“Baldwin”) is a registered investment adviser that does not suggest a certain level of skill or training. The views and opinions expressed in this newsletter are those of Baldwin professionals and may change at any time without prior notification. There is no guarantee that the objectives of any investment program will be achieved. Any strategies or securities discussed is not a recommendation to invest in such strategies or to purchase or sell securities. Investing involves the risk of partial or total loss that investors should be prepared to bear. Past performance is not a guarantee of future results.. The value of investments may be worth more or less than their original cost when sold. Baldwin obtains information from third-party vendors believed to be reliable; however, the accuracy of such information is not guaranteed. For additional information regarding Baldwin’s business practices, registration status and important disclosures, please click on the following link and type our name in the space provided IAPD – Investment Adviser Public Disclosure – Homepage (sec.gov)