OUR LABOR PUZZLE…….

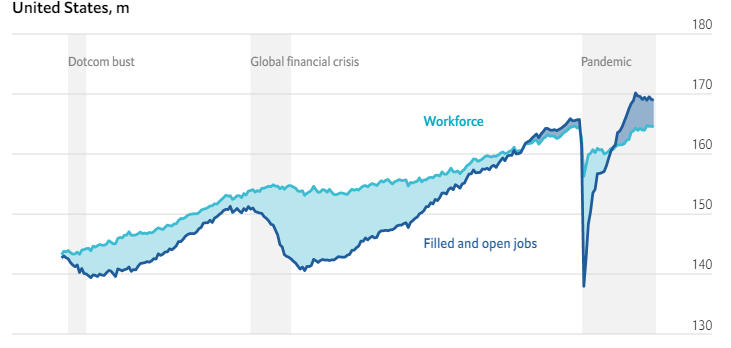

It has continued to be the case that labor shortages in too many businesses have been a major headache. “Tight” labor markets have led to higher payrolls and worker turnover, as well as decreasing productivity and persistent wage inflation, all of which have concerned central bankers. Monetary policy, once very loose, has tightened dramatically – negatively affecting equity and bond markets. What happened to the supply of workers during the pandemic? Chart 1 below shows that the workforce in the U.S. is essentially back to pre-pandemic levels (light blue line), but the demand for workers has increased by approximately 3 million positions (dark blue line), resulting in the gap on the far right of the chart representing about 3% of all those employed – hence the wage inflation. Reasons for the mismatch between supply and demand are several. But two of the most important are age and sickness.

CHART 1

Source: The Economist

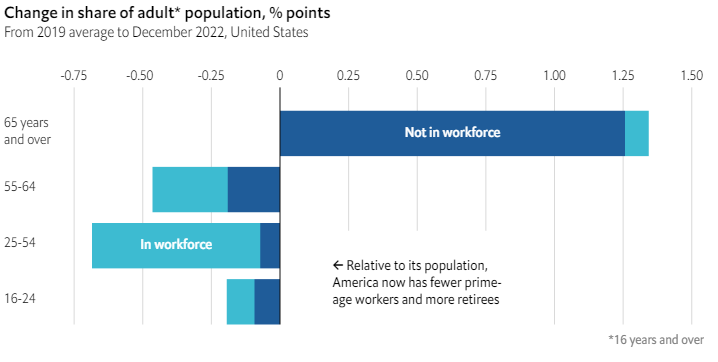

CHART 2

Source: The Economist

As can be seen in Chart 2 above, the number of people 65 years old and older has grown while other age groups have diminished in size. This aging of the population is calculated to have cost a loss of 1.9M workers for the American workforce. This graying of America will not stop.

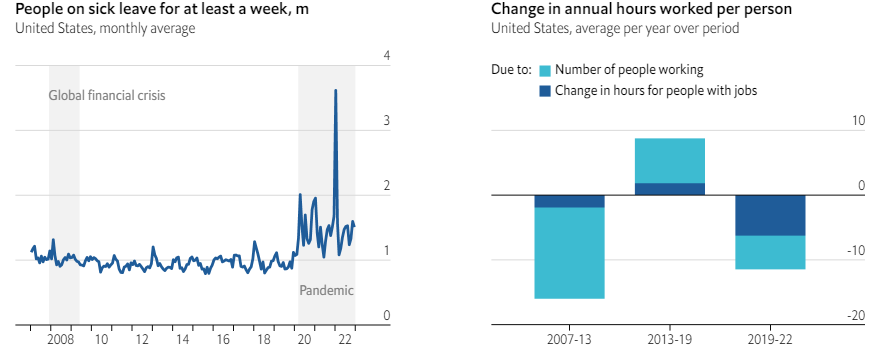

CHART 3

Source: The Economist

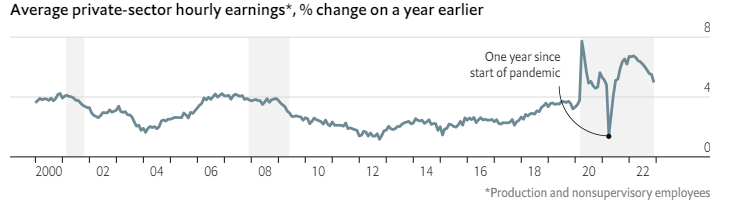

Illness is the other major reason for the labor supply/demand mismatch. As see in Chart 3 above, there was a huge jump in people falling ill during Covid – not at all unexpected. In 2022 an average of 1.6M Americans missed at least one week of work/month to recover from Covid, the flu, etc. – up from 1M before the pandemic. In contrast to the aforementioned aging dilemma, most people will get better. So, there will be and might already be some relief on the labor supply and the wage pressure from simply a healthier work force. Chart 4 below demonstrates this improvement with the hourly earnings curve bending down at the far right of Chart 4.

CHART 4

Source: The Economist

We repeat, however, the graying of America and the pressure it puts on wages will not go away.

MEASURE FORWARD, NOT BACKWARD…….

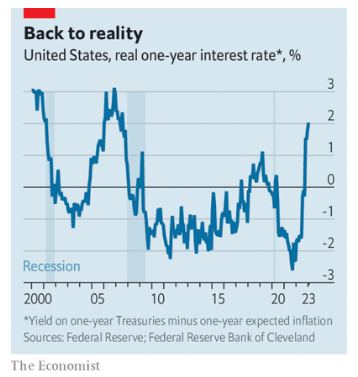

Almost invariably, the financial press calculates interest rates by subtracting an inflation measure like the current CPI (consumer price index) from an interest rate measure like the Fed funds rate or the 1-year Treasury rate. Presently, many analysts are fretting, for it shows a negative real return – i.e., the CPI is higher than the prevailing interest rate. Extrapolating from this result, analysts worry that the Fed will have to continue to raise interest rates to get them above the inflation rate so that investors get a real return on their money, with monetary policy remaining “tight” enough to slow the economy and dampen inflation. There is a flaw, however, in this calculation. The CPI or the PPI (Producer Price Index) are “backward” looking – they reflect past prices not future prices. Interest rates, on the other hand, do reflect future expectations – i.e., what will the cost of money be? Notably, if one were to substitute the CPI measure for gauges of inflation expectations which draw on more timely bond pricing and survey data, a very different result happens as shown in Chart 5.

CHART 5

Chart 5 clearly demonstrates that monetary policy is already tight. Interest rates net of expected inflation are currently a positive 2% and have climbed sharply over the past year, approaching a level of 3%, where recessions have started in the past. This could be another signal that the Fed might be just about finished its interest rate hiking for this cycle.

DIET FREE SERENDIPITY FROM OVERSEAS GETTING NOTICED IN THE U.S.…….

In 2020, two-fifths of the world’s population was considered to be overweight or obese. By 2035, according to the World Obesity Council, a non-governmental organization (NGO), that number could swell to more than half. Obesity can cause a host of health problems (i.e., diabetes, heart disease, stroke, gout, and numerous cancers) and is estimated to cost society $4 trillion by 2035 to deal with these diseases. The causes of obesity are multiple – ranging from personal genetics, environmental factors, an abundance of cheap, processed food, to a decline in exercise. Whatever the reason for someone being overweight, there are too many people in the world who are overweight and there is a huge societal cost connected with this condition.

CHART 6

Fortunately, lightning struck in the labs of Novo Nordisk, a Danish pharmaceutical. Novo for years had been a leader in diabetes research. After years of developing insulin, the company discovered a new class of drugs, GLP-1 receptor agonists. Semaglutide (Novo’s trade name for the GLP-1 receptor agonists) demonstrated in clinical trials that while helping diabetics, those patients, often with weight problems, lost weight – approximately 15% of total body weight. This happens because Semaglutide mimics the release of hormones that stimulate a feeling of fullness and reduce appetite. Already, Ozempic and Wegovy (commercial name for Semaglutide) are for sale internationally and competition from Eli Lilly and other pharmas is on the way. The market for these drugs is huge because they could help to solve a big societal problem. There should be some circumspection, however, as the use of these GLP-1 agonists has been brief, so the long-term side effects are not yet fully understood. These drugs are also not cheap. But they are cheaper than caring for diseases caused or exacerbated by obesity. Moreover, new competing drugs will no doubt drive down prices. From another perspective, it was the investors in Denmark’s Novo Nordisk who have benefitted enormously from this innovation, this serendipity. There are and will be interesting investment ideas from overseas and international investing that should be a part of a well-diversified portfolio.

LOWER ENERGY PRICES IN THE MIDDLE OF A WAR – BIZARRE…….

It was a year ago that Russia crashed through its border with Ukraine in an attempt to quickly overwhelm and annex its neighbor. That obviously did not work as we sit here today with the bloodiest war on the European continent since World War II still raging and with Russia having made little progress. Soon after the start of hostilities, oil prices soared and eclipsed $120/barrel. They now are trading at less than $80/barrel. Natural gas prices have retreated by almost 90% since last summer, approaching their lowest level since 2021. Fears were that the high energy prices would throttle European economies – and others as well. Contrarily, the lower prices for oil and gas have helped support the European and US economies.

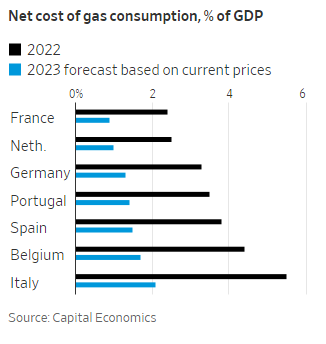

CHART 7

According to Capital Economics, declining natural gas prices equal cost savings of about 3.5% of Gross Domestic Product (GDP) for Italy, and 2% for Germany, Portugal and Spain. This energy savings swings Eurozone GDP from a contraction to slight growth – a large economic positive. Further, not having to face as huge as expected energy bills, puts consumers in a better frame of mind – i.e., more willing to spend on other things, which they have done.

CRACK…….SOMETHING JUST BROKE…….DEJA VU ALL OVER AGAIN……

Early March brought not only the Ides, but also another bank run. Despite the world having survived the Great Recession of 2008 – 2009 which was brought on by a bank run then and having dramatically strengthened banking rules to hopefully prevent that debacle from ever happening again, another mini-run on several banks has happened and resurfaced fears of the last time we all saw this movie. How did it happen? Since the banking rules were changed under Dodd-Frank legislation, parts of Dodd-Frank were subsequently altered in 2018, loosening regulations, easing capital requirements which allowed banks that were less than $250B in asset size certain freedoms not available to their larger competitors. These mid-sized banks were not deemed “systemically important”, with lobbyists arguing that they were not big enough to bring down the U.S. financial system and should be allowed to operate a bit more freely. While these institutions might not be the biggest, they were obviously big enough to rattle the markets. Poor balance sheet management practices and other idiosyncratic risks caused a rapid deposit flight within two banks (Silicon Valley Bank and Signature Bank) and they were quickly seized by the FDIC. Overseas and for completely different reasons (years of high-profile scandals and mismanagement), Credit Suisse, a systemically important bank in Switzerland, failed. Globally, investors and depositors started to squirm. In the span of less than a week, regulators, fearful of contagion, formulated strategies to support the banking system in both the U.S. and Switzerland. So far, it seems to have worked. Markets have settled. A result of this turmoil will inevitably be tighter credit. Banking officers will become more reluctant to lend. Consumers and corporations will hesitate to borrow. Deals will not get done. Equipment purchases will be postponed. The market will do a good measure of what the Fed was striving to do by raising interest rates. The U.S. economy will slow. A recession, which we could not identify heretofore, now becomes more possible – if not probable. There are still real strengths evident in the American economy, like very low unemployment, which will protect it in some measure. But this disturbance in the banking sector has shaken the financial system, which cannot be ignored.

A FINAL THOUGHT…

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

We recommend that you compare our statement with the statement that you receive from your custodian.

A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.