There has been a lot written about the ill effects of tariffs to be imposed on US businesses and ultimately the American consumer. Despite protestations from the White House, the vast majority of economists, industrial giant CEOs, tech CEOs, and most importantly small business owners (who by a wide margin employ most American workers) do not think the proposed tariffs out of Washington will be good for US business and their business, in particular. That story is written about almost daily and we are not going to spend any more ink on that angle here. Rather, we want to spend time looking at tariff effects on our trade “enemies” – as we have entered into this trade war. For our purposes, we want to focus on China, our third largest trade “enemy” and the one which seems to drive American trade ire.

Below, the reader will see three charts which quite clearly outline trade flows to the US, with a particular focus on Chinese imports in Charts 2 and 3. These statistics come from Vizion, which accesses millions of ocean container freight bookings daily via their Tradeview product.

CHART 1

CHART 2

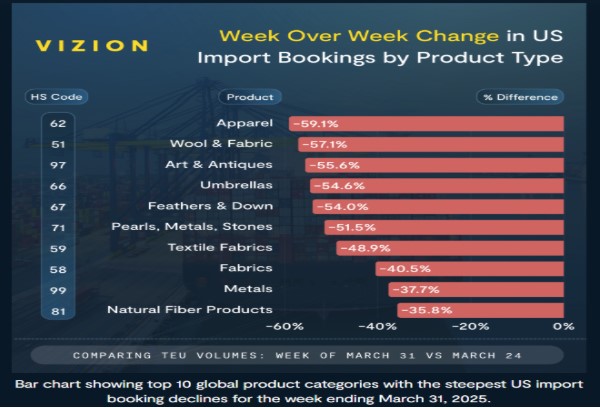

CHART 3

In Chart 1, a sharp falloff in trade started early in 2025 as the expected imposition of tariffs became more widely discussed in public and their contours were confusingly described. As tariff related uncertainty intensified, cargo booking volumes out of China continued to decline, and the effects of that uncertainty became even more evident in mid-April as demonstrated in Chart 2 in the far-right column. Week Over Week, Chinese exports to the US dropped by 22.14% and Year Over Year, Chinese exports to the US plummeted 44.49%. Finally, in Chart 3 is a sampling of the types of goods that have seen dramatic declines in orders from America: Apparel -59.1%, Wool & Fabric – 57.1%, Umbrellas – 54.6%, Textiles – 48.9%, etc. These are serious shortfalls in business. According to Gene Soroka, Executive Director of the Port of Los Angeles, “you’re probably going to see two-thirds of the normal cargo or less coming through the Port of Los Angeles in the weeks to come”. Data from Vizion and Dun and Bradstreet show that in the first week in April there was a 64% plunge in new bookings for shipments from China to the US. Reporting from China, the Economist magazine notes that the number of containers moving from Zhejiang factories to the port of Ningbo has slipped by one third. A vacuum parts manufacturer located in Ningbo is hoping to manage by shutting down some of his industrial robots because the firms his company supplies with parts have already laid off workers. Canceled orders have cost a Chinese plastics manufacturer $20 million. Goldman Sachs thinks that 16 million jobs in the export sector may be at risk in China if the trade war goes on too much longer. In response, the Chinese central government is trying to sell unsold goods elsewhere in the world – but not having much luck, as the rest of the world was already reeling from having too many Chinese goods on their shelves and has been pushing back like the US. The central government is also trying to sell the unwanted goods domestically – but again with little success because the Chinese consumer has pulled back, many being mired in the long-lasting real estate depression and trust banking debacle.

It appears clear that there will be pain – pain on both sides of this trade war. Washington has admitted it. The Chinese officially brush the loss of American markets off as a nuisance and declare that there are other markets to pursue. But the Chinese are suffering and people are in the streets protesting. With no social safety net and no jobs, quite a few Chinese are angry and the Communist Party is aware. President Xi is aware. Until this trade war is settled, no one is winning – everyone is losing. We hope that this exercise in brinksmanship does produce a winner and soon.

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosure.

Peter H. Havens, Chairman

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.