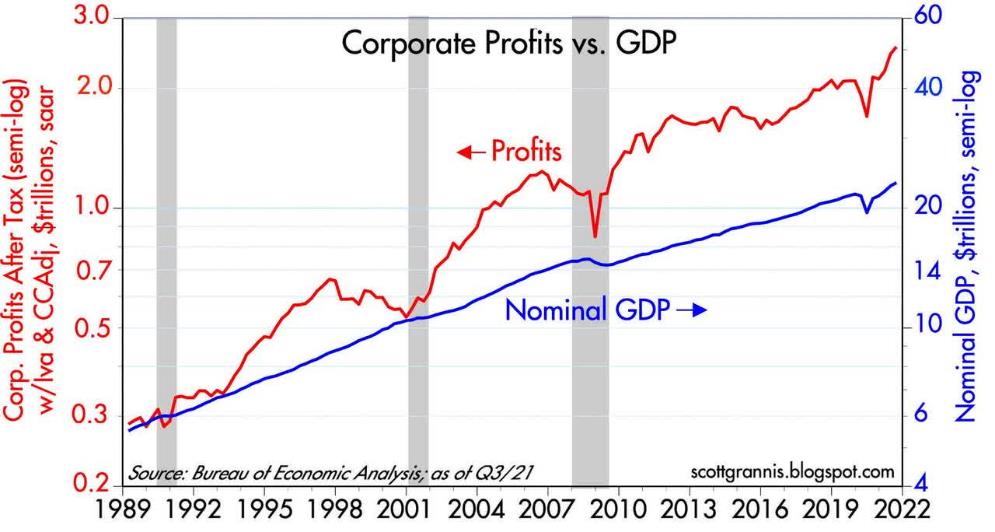

Net income and growing net income, this is the “heart” of our capitalist system. This is why entrepreneurs get up in the morning and go to bed late at night. Increasing cash flows which beget increasing profits which beget higher dividends, stock buybacks and higher stock prices in the marketplace – this is what drives the ecosystem of capitalist rewards, and U.S. corporate profits have been astounding. In Chart 1 below, company profits are measured vs. American GDP (Gross Domestic Product). Both are at all-time highs.

Chart 1

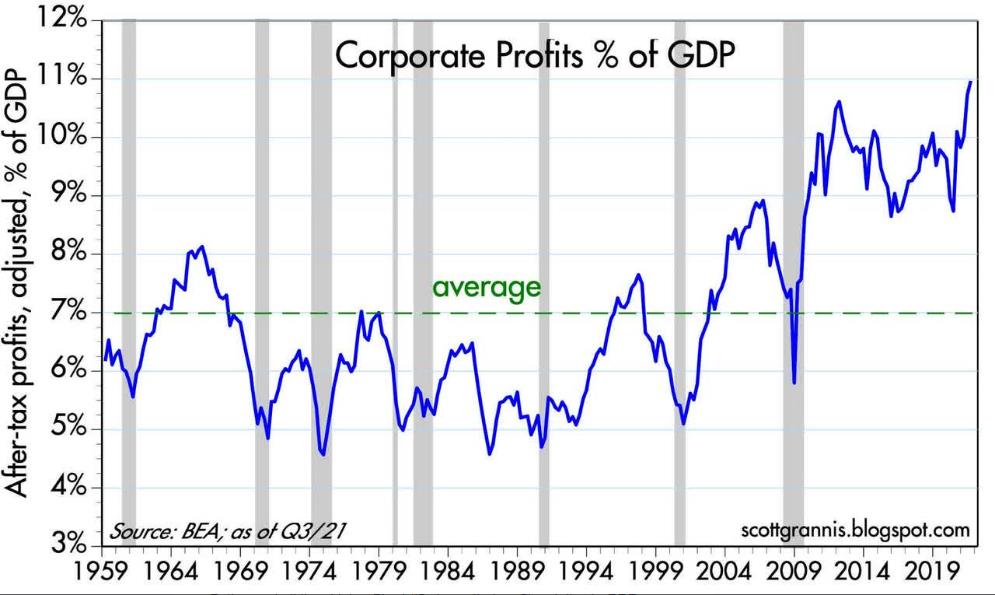

Corporate net income as a % of GDP is also at a record high.

Chart 2

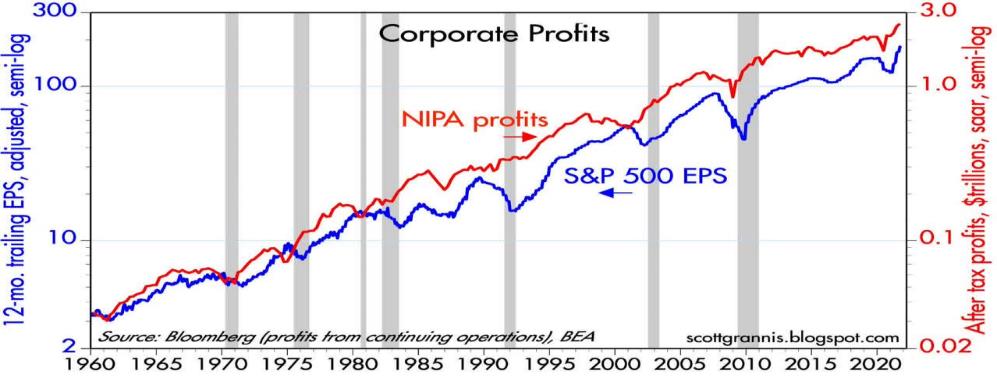

Finally, let’s look at two different but comparative calculations of profit which over time have tended to confirm one another – i.e., company profits as calculated in the GDP accounts (red line) and the S&P 500 trailing 12-month earnings per share. Note at the far right of Chart 3 that the lines have taken a sharp turn up, which suggests that corporate profits are going to continue to be impressive for some time.

Chart 3

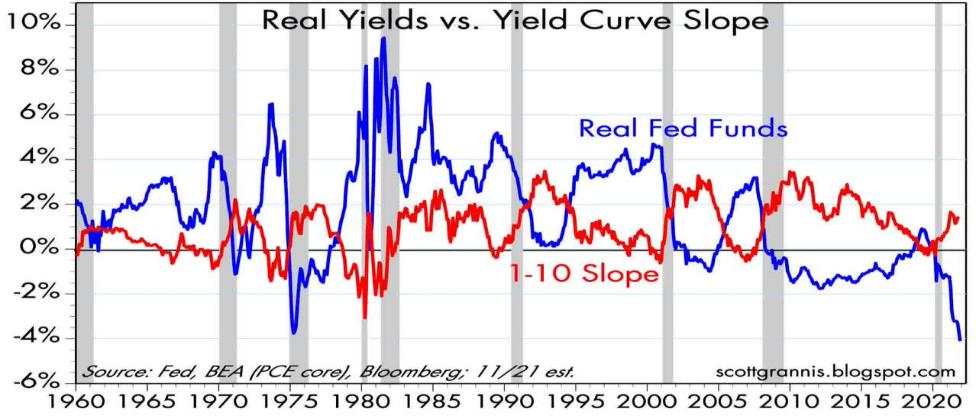

Is there any hint of a recession which might choke the economy and damage company performance? Every recession in the past 50 years (with the exception of the COVID pandemic-induced recession of 2020) has been preceded by a time of sustained monetary tightening – i.e., expensive money – as evidenced by high real interest rates (think an interest rate minus inflation) and a flat or inverted yield curve (think interest rates the same from 1 to 30 years’ maturities or higher interest rates for shorter maturities than longer ones). Let’s further look to the bond market, which prices money, to see how expensive or inexpensive money is today. In Chart 4 (next page), the reader will note that Real Fed Funds are negative currently (very cheap money) and there is some slope in the yield curve from 1 – 10 years, indicating no recession, according to the bond market. So, with no recession projected, company earnings should continue to march ahead.

Chart 4

OK, BUT WHAT ABOUT INFLATION????

Inflation is an important determinant of market prices because inflation influences bond pricing through interest rates. If inflation rises, interest rates eventually will rise, bond yields will increase, and equity prices may fall if bond yields rise too much.

Chart 5

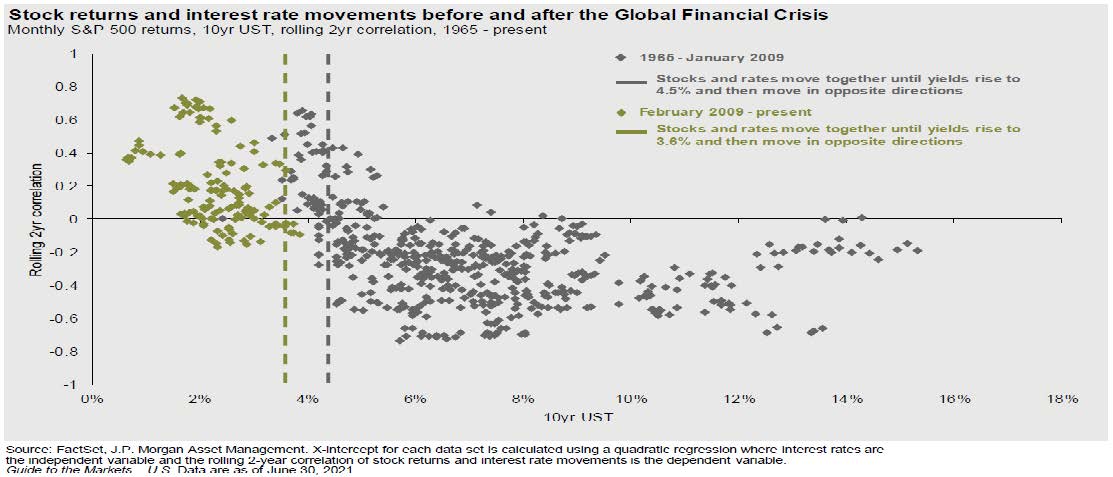

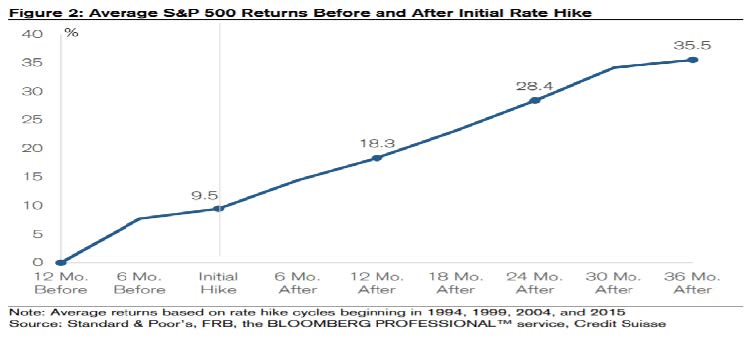

We have used the previous chart in the past because it illustrates well the competitive interrelationship between interest rates and stock prices. According to work done by JP Morgan, the 10-year Treasury yield would have to eclipse 3.6% (currently 1.44%) for U.S. equity prices to falter. So far, stock prices are well supported by low interest rates as the bond market does not seem yet to be concerned about inflation. Further, according to Credit Suisse, history shows that stock returns remain robust in the months preceding and following the Initial rate increase.

Chart 6

So even if interest rates go up, it will not necessarily be the end of the stock market rally. For the past decade at least, interest rates have been on a steady decline because inflation has been on a steady decline. Globalization of service and product flows have enabled companies through much improved information technology to bend pricing curves down because there has always been another producer or vendor willing to sell a service or product at a cheaper price. These global and technological forces are still at work today. They are embedded in corporate cultures. This does not mean that in the short run (say up to a year) during a transition from recession to expansion the U.S. economy might not avoid inflationary pressures due to logistical “glitches”. In fact, strong demand for goods like autos, furniture and appliances has driven much of the current inflation surge. Prices for services, such as for travel and recreation, have climbed much less with softer demand. We concede that inflation has shown itself because of inefficiencies during the economic re-start in 2021. But given time, the world’s trading system should recapture its former efficiency and continue to cap price pressures. We also share this belief of lower future inflation with the Fed. The Federal Reserve has a staff of 400 Ph. D economists – more than any bank on Wall Street by a wide margin. This deep knowledge base has allowed the Fed to examine economic minutiae which most economists ignore for they do not have the time. Academic papers from the European Central Bank and research co-authored by Christina Romer, a former Chair of the Council of Economic Advisors, have substantiated that Fed staff forecasts are more accurate than private forecasts. Right now, the Fed believes that inflation will be lower in 2022 than in 2021. So that’s the direction we are leaning. However, as time has gone on, this has become a position which is not without controversy. For a while, the Fed described the current inflation as “transitory”. That term has now been “retired”. While the Federal Reserve has already outlined a timeline over the next year as to when it will finish its quantitative easing (think bond buying) it is supposed by quite a few market watchers that this timeline will be moved up and that perhaps the first increase in interest rates will also be accelerated from 2023 to late 2022. So as new information comes to the fore, reactions to that information may well change. We still think inflation in 2022 will be lower than it is today – but the Fed may well become “tighter” in its monetary policy a bit sooner than earlier thought, in order to prevent an inflation rate far above its stated policy rate of around 2% as measured by the PCE (Personal Consumption Expenditure index).

THEN THERE’S INTERNATIONAL UNCERTAINTY….

Two major “flashpoints” loom large in our mind – Russia and China. As this is being written, Russia is massing tens of thousands of troops and tons of materiel on its borders with the Ukraine – indeed a menacing sight. Further, Russia has already invaded the Ukraine in 2014 seizing the Crimea and parts of the Donbass. Certainly, Russia could be serious about an attack, despite their protestations otherwise. And clearly Russia might be emboldened to “take another swipe” at its neighbor because the last time they did so, the repercussions, while painful, were not painful enough. This time however the U.S. and its European allies seem to be more determined to stand their ground. From news reports and conversations with some “informed friends”, it would seem that Russia is being warned that any attack would bring a coordinated economic, diplomatic and military response from America and its European allies. Economic sanctions would be strengthened; broadened and targeted at close personal allies of President Putin and Putin himself. In other words, besides disrupting Russian corporate trade, these sanctions would go to grab the money in foreign banks outside of Russia which Putin and his friends have “squirreled away”. Diplomatically, Russia would be even more of a pariah than it is today. International deals would become very difficult to accomplish. Militarily, NATO would probably send troops to former members of the Soviet state (think Estonia, Latvia, Romania, Poland, etc.) which are now members of NATO and bring “hostile” troops closer to the Russian border than they are today, which would enrage Putin and seem counterproductive to his proclaimed goal of getting NATO troops farther away from Russia. Finally, the U.S. could use an economic “nuclear” option – disconnect Russia from the Swift (Society for Worldwide Interbank Financial Telecommunication) international payment system used by banks around the world. This would be a devastating blow, bringing the Russian economy to its knees. Russia could be characterized as a “gas station with nuclear weapons”. It is because of its nuclear weaponry that the world takes any notice of Russia. It is economically weak with precious little to sell to the world that the world wants – except for oil and gas. Happily today, there are numerous alternate sources of hydrocarbons and the world is working hard to replace hydrocarbons as fuel. So, Russia is a worry – but not for today, we believe.

China is also a worry – but as with Russia, we do not think for today but could well be as early as 2023. As opposed to Russia, China has a very strong and large economy. It can endure economic storms and while buffeted by harsh conditions, China can withstand economic punishment. It also has a very large and modern military which has been built up over the last several decades, but especially in the last 10 years. And while China has large forces – they are not battle tested. The last time the Chinese were in any sort of a pitched battle was during the Korean War, some 60 years ago. Under President Xi, China has become much more outward looking, confident of its capabilities and eager to become a force at the “top table”. It demands respect internationally and rejects interference from other nations in areas which China deems its sphere of influence or matters which the Chinese think of as internal. China will not “kowtow” to others. In 2022, Beijing will host the Winter Olympics. Later in the year, President Xi aims at the 20th Communist Party Congress to direct the Chinese Communist Party (CCP) to re-appoint him for another 5-year term as President – his third – which would be unprecedented in modern Chinese political history. Also, at the moment, the government is having to deal with the default of Evergrande, the second largest real estate developer in China. Real estate development generates about 30% of Chinese GDP. Having the second largest entity of the most important industry in the country going “belly up” is a very big worry because of fears of economic contagion spreading elsewhere in the economy. Certainly, President Xi does not want the Chinese economy to go bad on his “watch” – especially when trying to convince other members of the CCP that he should get another term in office. While there have been hard words about Taiwan and provocative flights by the Chinese air force into Taiwanese airspace, we do not think that 2022 would be an auspicious time for President Xi to use military force to force a final solution for the Taiwan issue. Why is Taiwan even an issue for the U.S. as it is halfway around the world? Simply stated, Taiwan is where there is a concentration of semiconductor manufacturing capacity – both sophisticated and simple. There is no other location in the world with Taiwan’s capabilities or capacity. If China were to attack Taiwan, damage and/or then control the world’s predominant semiconductor manufacturing capacity, the world would go into a severe recession. Any attack would galvanize southeast Asia against China. Japan, Australia, India and the U.S. would join forces to defend the status quo. Militarily, China would have to fight not only those four but also Viet Nam, the Philippines and South Korea in addition to a very “prickly” Taiwan whose military forces, while not large, are skilled and fighting on their own soil.

Diplomatically, the Chinese would be ostracized. Economically, while in a much better position than the Russians, having most of the world turn away from China would make it hard for the country. And in much the same way as with Russia, there is always the economic “nuclear” option of disconnecting China from the Swift international payment system. That would be a body blow. China’s moving aggressively on Taiwan we think is a real worry and give it better odds of occurring than Russia’s moving on Ukraine. But we believe that 2022 would not be the right time.

WHEN WILL POST-PANDEMIC BECOME REALITY?

Great medical strides have been made to combat COVID. Very effective vaccines are widely available and new, very effective therapeutics developed by Merck and Pfizer have been approved by the FDA which should make it even easier for people to protect themselves. Nevertheless, according to medical experts, variants of COVID develop in those who are unvaccinated and the tens of millions who are unvaccinated provide a “fertile field” for virus mutation. These variants complicate full recovery of the world’s economy because upon the appearance of a new variant, the world hesitates – asking “will the current vaccines work?” Thus, while studies are launched to see if current vaccines are effective against a new strain of COVID, people step back and the world shudders. It will not be, according to every medical expert to whom we have spoken, until more people get vaccinated that we will achieve herd immunity and we can finally use the hyphenated word “post-pandemic” as a descriptor. We think (hope) this should happen in 2022.

SO WHAT DO WE THINK ABOUT MARKETS?

In the U.S., the fixed income markets will have difficult times because the Fed has already put investors on notice that rates will be rising in 2022. This would clearly suggest that investors should stay short with duration, so that when short maturity bonds mature, the proceeds can be reinvested in higher yielding securities. The U.S. stock market should have earnings underpinning prices and not have too much of a “headwind” from slightly higher interest rates. But higher interest rates will put pressure on P/E ratios. While we expect earnings to rise, we think P/E ratios will fall and thus do not expect as buoyant a stock market in 2022 as we had in 2021. Overseas equity markets will have a difficult time competing with higher U.S. interest rates. Counterbalancing that will be valuation, as overseas markets remain severely undervalued vs. the American markets. We still like international names in both developed and emerging markets. International bonds, like their American counterparts, we think will be challenged. Some countries are already raising rates while some are hesitating. In any case, it will be hard for international bond markets to go in a different direction from the U.S. bond market. If the U.S. is raising rates, eventually all others will have to raise rates – because the U.S. bond market is just too big to ignore.

We at Baldwin wish you the happiest of New Years…

PREDICTIONS – HOW DID WE DO IN 2021?

- Inflation will stay low. No – Logistical “hiccups” & labor issues put “sand in the economic gears.”

- Interest rates will remain low. Yes

- The dollar will weaken. No

- Oil will stay in a pricing range of $50-$60/bbl. No – Good demand & supply discipline have kept prices stronger than anticipated.

- World GNP (Gross National Product) will rebound strongly. Yes.

- Corporate earnings will rebound strongly. Yes – Very Strong.

- Investor “risk appetites” will increase. Yes.

- International equities will outperform U.S. equities. No.

- In the U.S. infrastructure spending will jump. Yes – A little delayed, but happening.

- U.S. stocks will have a good year and some rotation out of “tech darlings” into more economically sensitive names. Yes.

PREDICTIONS FOR 2022

- Interest rates to rise a bit in 2022.

- The dollar will be firm.

- Corporate earnings will be strong – but not grow as fast as in 2021.

- U.S. infrastructure spending will take off.

- China will continue to threaten Taiwan, but not move on Taiwan.

- Russia, after lots of “saber rattling”, will back away from Ukraine.

- Oil will stay well priced.

- Inflation will “simmer down” from closing 2021 levels.

- Investor “risk appetites” will stay strong.

- U.S. Stocks will continue to make progress – but more subdued than in 2021.

A FINAL THOUGHT

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

We recommend that you compare our statement with the statement that you receive from your custodian.

A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmanagement.com/disclosures.