Introduction

Continuing our exploration of GLP-1 weight-loss drugs (GLP-1 Part 1) https://www.baldwinmgt.com/glp-1-weight-loss-drugs-overhyped-or-a-gamechanger/ , we will review recent developments that further boost credibility and excitement about the GLP-1 class of drugs, with advances in scientific understanding, as well as updates on recent late-stage trial successes and insurance coverage progress. We also will introduce the drugmakers, including the formidable duopoly of Novo Nordisk and Eli Lilly, as well as some of the challengers.

Recent Developments

GLP-1 drugs have been proven to be powerful modulators of appetite, but drug researchers are trying to better understand exactly how they work. Secreted by the intestines after eating, the naturally occurring gut hormone GLP-1 is broken down by enzymes in the body within minutes. While considered a “gut” hormone, the GLP-1 hormone also is secreted by neurons located in the hindbrain at the base of the skull, interacting with GLP-1 receptors throughout the rest of the brain. As patients take GLP-1 medication, these synthetic hormones flood the bloodstream, permeating the body, penetrating deeply into the brain and suppressing the appetite. Further, as some scientists better understand the crucial brain connection, they are exploring whether addictive/compulsive behaviors as well as diseases with a theorized inflammatory connection such as Alzheimer’s and Parkinson’s disease may effectively respond to the GLP-1 drug class. Intriguingly, the most common complaints/side effects afflicting GLP-1 drug users are nausea and vomiting, and scientists have recently identified the brain area/receptors in rodents wherein GLP-1 drugs can suppress appetite without causing these unpleasant side effects. This would be the biopharmaceutical “holy grail” if a future targeted drug formulation could duplicate these findings.

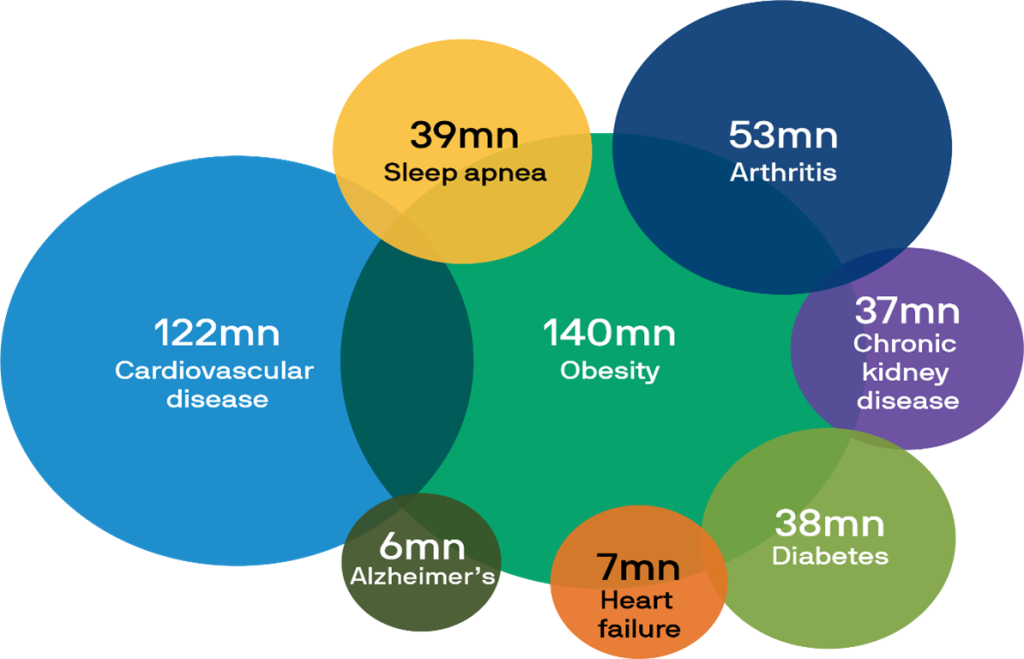

Thus, the “race is on” among biopharmaceutical companies to develop drugs with the optimal combination of weight loss, minimal side effects, ease of production and use, and most importantly, the ability to mitigate or even cure a variety of serious chronic diseases. See Chart 1 below:

Chart 1- U.S. population suffering from chronic diseases that may respond to GLP-1 drugs:

Source: Alzheimer’s Association, American Diabetes Association, American Heart Association, Centers for Disease Control and Prevention, Journal of Cardiac Failure, National Council on Aging, National Institute of Diabetes & Digestive & Kidney Diseases, World Obesity Federation, J.P. Morgan Asset Management; as of January 2024.

Drugmakers have aggressively launched trials studying GLP-1 drugs’ potential to treat a wide variety of chronic health conditions. Below is a selection of recent drug trial results:

- In March of 2024, the FDA approved Novo-Nordisk’s Wegovy as a treatment to reduce heart disease risks in overweight and obese adults following the release of trial data from the previous fall: a five-year 17,600 patient study showed that overweight people with existing heart disease reduced their incidences of strokes, heart attacks and other heart-related complications by 20%. Improved health outcomes were evident before patients lost weight. A more recent study highlighted the heart-protective benefits of Wegovy, regardless of the patients’ starting weight or how much weight was lost over time.

- Also in March, a study demonstrated that Wegovy cut the risk of kidney disease-related events in people with Type 2 diabetes and chronic kidney disease by 24%.

- In April, drugmaker Eli Lilly announced that its dual receptor GLP-1/GIP drug Zepbound reduced the severity of obstructive sleep apnea by 63% (about 30 fewer events per hour) in overweight adults in two separate late-stage studies.

- Also in April, the New England Journal of Medicine released the results of another Wegovy trial in which patients with Type 2 diabetes and a common type of heart failure (preserved ejection fraction) experienced a significant reduction in heart failure-related symptoms and physical limitations. They lost about one-half the weight as compared to participants in other trials. However, Dr. Mikhail Kosiborod, a cardiologist at Saint Luke’s Mid America Heart Institute and the lead doctor of the study noted, “It’s not all about weight loss,” adding that semaglutide (Wegovy) is “fundamentally modifying the disease process.”

- In early June of 2024, Eli Lilly announced the results of a Phase II trial demonstrating that its Mountjaro GLP-1 class drug effectively treated patients suffering from MASH, a serious metabolic liver disease.

Clearly, the GLP-1 drug class is not just about weight loss. These versatile drugs have the potential to treat a vast array of serious diseases. But what about the two “elephants in the room”, insurance coverage and costs?

Notably, the American Medical Association classified obesity as a disease in 2013. Despite this, Medicare is restricted from covering weight-loss medications unless they are prescribed to treat a separate medically accepted indication. New ground was broken a couple of months ago when Medicare agreed to cover Wegovy for participants with heart disease based on the trial results summarized above. As compelling trial data for additional indications are released, analysts expect Medicare to widen the door to coverage. Commercial insurers also are increasing coverage. In fact, Eli Lilly remarked that the insurance coverage of its weight-loss drug Zepbound reached 67% of patients during the most recent quarter. JP Morgan analysts expect that level to rise to 80% in short order. However, there has been some highly publicized pushback. Earlier this spring, North Carolina controversially announced that it was discontinuing the coverage of various GLP-1 weight-loss drugs for its state employees because of the high costs. This is the biggest “elephant”: can society afford these drugs? To set the stage, a comprehensive study by Oppenheimer from last fall entitled GLP-1’s: Miracle or Mirage stated the following:

The statistics in the US (compared to the rest of the world) are even worse, with ~42% of the population technically classified as obese or super-obese, and ~$1.8T/year being spent simply on obesity-mediated conditions and complications. Recent estimates for 2030 predict that, if left unaddressed, the prevalence of adult obesity in the US will reach ~50%, and nearly 25% will have class 2 obesity (BMI ≥35 kg/m2). On average, healthcare costs for an obese person are ~$4,000/year extra vs. a normal-weight individual. Indirect costs of obesity from lost productivity, etc. are 2-3x of direct costs. The obesity trajectory is headed to an unmitigated disaster, from both a health and economic perspective.

Despite these worrisome factors, GLP-1 drugs are still expensive at roughly $12,000/year/patient, quite a burden for governmental and commercial insurers. However, expecting an upsurge in competition, with roughly 124 drugs in development in pre-clinical to late-stage clinical phases, along with the imminent rise of more efficiently and cheaply produced oral GLP-1 drugs easing current supply shortages, and intense pharmacy benefit management negotiations, the costs of these drugs will drop over time.

GLP-1 Drugmakers

Goldman Sachs recently predicted that annual sales of GLP-1 drugs could equal or exceed $130 billion by 2030. Currently, two large biopharmaceutical companies are the first movers: Danish company Novo-Nordisk and US company Eli Lilly. Both pioneered the development of insulin to treat diabetes over one-hundred years ago and are accustomed to being rivals in what is currently a GLP-1 duopoly. These two companies have an “underappreciated moat” according to JP Morgan analysts, who add that multi-billion-dollar capital requirements for drug development and manufacturing, a significant reimbursement wall given high sales that make payer access a challenge for newer entrants, and deep pipelines with a myriad of drug candidates which will monopolize trial resources, combine to perpetuate these companies’ dominance and restrict challenger market share to less than 10%.

Novo Nordisk (Novo) and Eli Lilly’s (Lilly) stock prices have risen by over 81% and 89% over the past 12 months. Both have relatively high valuations from a price/earnings perspective at 35 and 51X earnings expectations for the next 12 months. Despite these rich statistics, their anticipated growth trajectories significantly dwarf their industry peers.

What about the challengers? In March, Viking Therapeutics’ stock price exploded, driving the market cap to $8 billion, after trial results from early stage GLP/GIP drugs showed potentially superior results to some of Lilly’s and Novo’s drugs. Analysts were tripping over each other to make extravagant sales projections for a money-losing company with no approved drug candidates. Importantly, neither Novo nor Lilly is standing on its laurels as a complacent early mover. It is quite possible that Viking ultimately will be acquired by a larger rival.

Amgen was in the news earlier this month when CEO Robert Bradley expressed that he was “very encouraged” by mid-phase results from its GLP-1 candidate MariTide, especially since it is injected 1x/month rather than a 1x/week as is the current standard. The stock immediately rallied by 16%, despite no new data being released. Again, Lilly and Novo both are developing oral drug candidates as well as drugs requiring less frequent subcutaneous injections.

What about a fund option, encompassing both the incumbents and the challengers? The alternatives are few. Tema Obesity and Cardio Metabolic ETF(HRTS), launched this past November, and a recently introduced Roundhill GLP-1 and Weight Loss ETF (OZEM) are the only ways to currently gain exposure via a fund. HRTS’s current market value is $62 million. Its management fee is .75% during the early days but the plan is to raise it to .99% of assets under management. The fund currently invests in about 40 stocks, with 5%+ weightings in Novo and Lilly, along with many smaller companies like Viking Therapeutics. Amplify also has filed a prospectus to launch a fund imminently (Q2 2024). The Amplify Fund is expected to invest in about 20 stocks, whereas the Round Hill ETF is expected to be more concentrated with fewer holdings. Given the small size and newness of this fund class, investing is premature.

Investors may want to consider the incumbents, Novo Nordisk and Eli Lilly. Both have done extremely well, but the majority of their growth is still ahead. Both companies are highly diversified with strong franchises and pipelines outside of GLP-1 drugs. In closing, a Goldman Sachs report recently compared Novo Nordisk and Eli Lilly’s innovations with Amazon and Apple, saying they “have the opportunity to expand into categories far beyond what most investors are currently contemplating.”

As every investor’s situation is unique, if you have questions or are interested in how to best position your investment portfolio to take advantage of these groundbreaking treatments, please reach out to your portfolio manager or any of us at Baldwin.

Sources:

- https://www.economist.com/science-and-technology/2024/03/30/could-weight-loss-drugs-eat-the-world

- https://www.theatlantic.com/health/archive/2024/03/ozempic-glp1-weight-loss-brain-gut/677645/?gift=DD-B4qmlYEVSbhv7uOdw5qQ-M1RmsnNPFt2LX3nnv-Y&utm_source=copy-link&utm_medium=social&utm_campaign=share

- https://www.bloomberg.com/news/features/2024-01-26/zepbound-how-eli-lilly-s-lucky-break-fueled-a-600b-weight-loss-empire?utm_source=website&utm_medium=share&utm_campaign=email

- https://www.washingtonpost.com/business/2024/03/08/wegovy-heart-disease-fda/

- https://www.marketwatch.com/story/wegovys-heart-benefits-are-not-just-linked-with-weight-loss-new-study-suggests-1bfcf903?reflink=mw_share_email

- https://www.usnews.com/news/health-news/articles/2024-03-22/medicare-to-cover-wegovy-when-patients-also-have-heart-disease

- https://www.axios.com/local/raleigh/2024/03/07/pushback-after-nc-cuts-its-weight-loss-drug-losses

- https://am.jpmorgan.com/us/en/asset-management/adv/insights/portfolio-insights/equity/glp-1s-more-than-just-obesity-drugs/

- https://www.marketwatch.com/story/big-pharma-is-looking-to-fatten-profits-with-buyouts-of-weight-loss-drug-companies-here-are-4-candidates-6ffe2550?reflink=mw_share_email

- https://www.kff.org/medicare/issue-brief/

- https://www.investors.com/etfs-and-funds/etfs/weight-loss-drugs-feisty-rivals-take-on-eli-lilly-novo-nordisk/

- https://www.bloomberg.com/news/articles/2024-05-03/here-are-the-obesity-drug-hopefuls-vying-to-unseat-lilly-novo

- https://www.reuters.com/business/healthcare-pharmaceuticals/wegovy-weight-loss-sustained-four-years-trial-novo-nordisk-says-2024-05-13/

- https://seekingalpha.com/news/4111624-goldman-sachs-raises-obesity-drug-market-estimate

- https://www.prnewswire.com/news-releases/lillys-tirzepatide-was-superior-to-placebo-for-mash-resolution-and-more-than-half-of-patients-achieved-improvement-in-fibrosis-at-52-weeks-302167649.html

- www.oppenheimer.com

- www.jpmorganmarkets.com

- https://www.lilly.com/

Baldwin Management LLC. (“Baldwin”) is a registered investment adviser that does not suggest a certain level of skill or training. The views and opinions expressed in this newsletter are those of Baldwin professionals and may change at any time without prior notification. There is no guarantee that the objectives of any investment program will be achieved. Any strategies or securities discussed is not a recommendation to invest in such strategies or to purchase or sell securities. Investing involves the risk of partial or total loss that investors should be prepared to bear. Past performance is not a guarantee of future results.. The value of investments may be worth more or less than their original cost when sold. Baldwin obtains information from third-party vendors believed to be reliable; however, the accuracy of such information is not guaranteed. For additional information regarding Baldwin’s business practices, registration status and important disclosures, please click on the following link and type our name in the space provided IAPD – Investment Adviser Public Disclosure – Homepage (sec.gov)

Susan Berry-Gorelli serves as the Chief Executive Officer of Baldwin Management LLC, and also is the Director of Research and a Portfolio Manager of Baldwin Investment Management. She has over 30 years of individual and institutional investment and risk management experience in the financial services industry. Susan attended The College of William and Mary and the University of Delaware, earning a B.A. in Economics and History, Summa Cum Laude and Phi Beta Kappa. She is the Board Vice President of the Colonial Theatre in Phoenixville, as well as serves on the finance committees of the French and Pickering Conservation Trust and the Whitemarsh Boat Club.