Shortfalls of numerous products and materials have “thrown sand into the workings of manufacturing” around the world and has led to increases in inflation numbers, upsetting central bankers and investors. For example, the semiconductor shortage has been well publicized. Auto makers have had to close plants for extended periods due to a lack of semiconductor supply. How did this happen? One of the marvels of globalization is “just-in-time manufacturing” – a strategy fully embraced by auto companies around the world. This is a manufacturing philosophy which embraces lean inventories of materials needed to make an end product and a dependence on a “well-oiled” logistical system designed to deliver necessary components to the factory gate just as the part is needed in the manufacturing process. This way of producing goods cuts inventory costs, speeds inventory “turns”, reduces capital investments, strengthens corporate balance sheets, and enhances company profitability. There is nothing in this list of attributes regarding just-in-time manufacturing that a corporate CFO and CEO do not like – except that it must run smoothly. If there is a “hiccup” as happened during the pandemic, then things do not run smoothly and costs go up. At the beginning of the COVID scare, auto manufacturers, fearing having too large an inventory of semiconductor chips for cars they would not produce, cut back their orders. At the same time, semiconductor orders exploded for other uses (think video games, music devices, home office equipment, etc.) that people were using during their stays at home. Then due to success in controlling COVID and further success with the vaccines, economies began to re-open, generating demand from customers for cars and from the auto manufacturers for more semiconductor chips. Unfortunately for the car companies, once they gave up their place in the “chip procurement” lines, they have had to scramble to secure the needed supplies. This scramble has not worked well in the immediate term – costs have risen, and plants have had to shut. In time, everything will return to equilibrium. But the pandemic has well demonstrated the “weak link” in just-in-time manufacturing. It is a complex logistical process which is delicately balanced when operating at maximum capacity. Just-in-time manufacturing leads to great efficiency – but is lacking resiliency. Without resilience, an efficient process can become inefficient (i.e. plant shutdowns) and very costly. Hopefully manufacturers who have wholeheartedly embraced just-in-time will “back off” a bit and re-introduce more flexibility (i.e. carry more inventory) to their manufacturing process to avoid the higher costs they are suffering now.

A COUNTERBALANCE

Combating inefficiency created by “sand in some manufacturing gears” is heightened worker productivity. From January to March of this year, labor productivity increased 4.1% year over year – the fastest in a decade. In other words, the U.S. economy is producing more units of a good or service per hour than it was, which pushes costs down. Now it is not unusual in the early days of an economic recovery for worker productivity to rise as employers are reluctant to hire and work to squeeze more sales out of every worker. As they emerge from the pandemic, it seems that companies have intensified their use of technology to better leverage their workforce. Industries like retailing, finance, construction, professional and business services – accounting for nearly one third of the job losses during the pandemic – have increased output. Software investments rose 10.5% in Q1 2021 year over year as businesses invested in cloud computing, collaboration tools and e-commerce. So while US GDP (gross domestic product) growth has been robust recently, job growth has not snapped back nearly so sharply, as can be seen in the chart below.

But importantly, productivity is up demonstrably, which will hold down inflation.

ONE LAST POINT TO MAKE…

We have recently seen snippets of data which suggest that there is indeed some inflation out there in the world. A goodly measure of this price resurgence we would argue is from temporary logistical difficulties, as described above. It is always the case when anything dramatically changes course, like the world economy coming out of a pandemic, inefficiencies will “creep into the system” and prices will temporarily increase. But we should all keep in mind the base from which those prices are rising. Please remember that for years, central banks around the world have been fighting disinflation and have feared outright deflation. The bankers have tried for years to spark inflation with no success. This has been because very powerful disinflationary forces like the globalization of labor and the internet have worked relentlessly to lower costs. Those forces are still alive and well today and in the case of the internet, we would argue, are even more powerful today than pre-pandemic as the pandemic made us all more dependent on the virtual realm than we were two years ago.

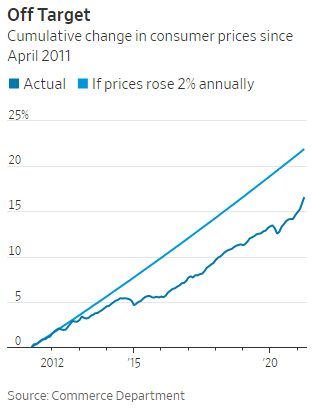

The “inflation goal” as stated by the US Federal Reserve and several other central banks is 2%. In the chart above, the reader will note that the actual inflation rate as measured by the CPI since 2011 has been and is well below the targeted rate of 2%. To get the US to the 2% line is going to take a lot more inflation than we have seen so far and for a much longer period of time than we have had so far. Counterbalancing the inflation bump that we have witnessed are the disinflationary forces which have held inflation down for years and have not gone away.

PREDICTIONS FOR 2021

- Inflation will stay low. Yes – Snippets of increase which we think are temporary.

- Interest rates will remain low. Yes.

- The dollar will weaken. Yes/No – Trend is generally down, but not in a straight line.

- Oil will stay in pricing range of $50-$60/bbl. No – Oil has rallied above $70/bbl with OPEC+ discipline & reopening demand.

- World GNP (Gross National Product) will rebound strongly. Yes.

- Corporate earnings will rebound strongly. Yes – Surprisingly so.

- Investor “risk appetites” will increase. Yes – Still believe.

- International equities will outperform U.S. equities. Yes/No – It has been a “seesaw” trade so far this year.

- In the U.S. Infrastructure spending will jump. Yes – Still believe, but Biden plan is “hung up” in Congress.

- U.S. stocks will have a good year with some rotation out of “tech darlings” into more economically sensitive names. Yes.

A FINAL THOUGHT

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

We recommend that you compare our statement with the statement that you receive from your custodian.

A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmanagement.com/disclosures.