U.S. and global economies are evidencing a strong economic recovery unfolding as people around the world get back to work. Data firm IHS Markit recently reported that its April Services Index for the U.S. rose to 63.1 (a mark over 50 suggests economic growth) from 60.4 in March – signaling the fastest expansion in 11 years. In manufacturing, the Purchasing Managers Index (PMI) climbed to 60.6 vs. 59.1 in March. In China, first quarter Gross Domestic Product (GDP) growth was +18.3% year over year and retail sales were +34.2% year over year in March. In the Eurozone, the April Composite PMI, which combines scores from manufacturing and services businesses, rose to 53.7 vs. 53.2 in March. Economic growth seems to be back and this is being reflected in equity and bond markets around the world – with stocks going up in price and bonds going down.

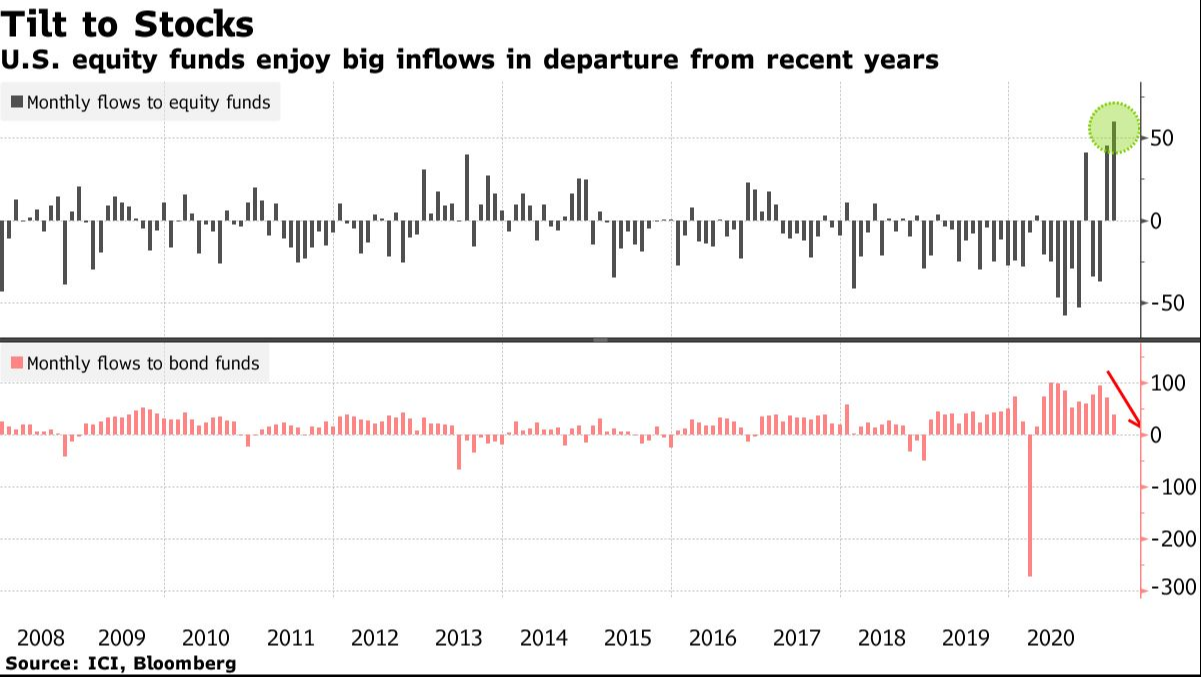

Investor money flows are highlighting signs that an alienation among fund investors towards bonds may be taking hold. In March, investors put approximately $20 billion(B) more into stock funds than they did into bond funds. This was the biggest inflow gap for equities since 2016.

CHART 1

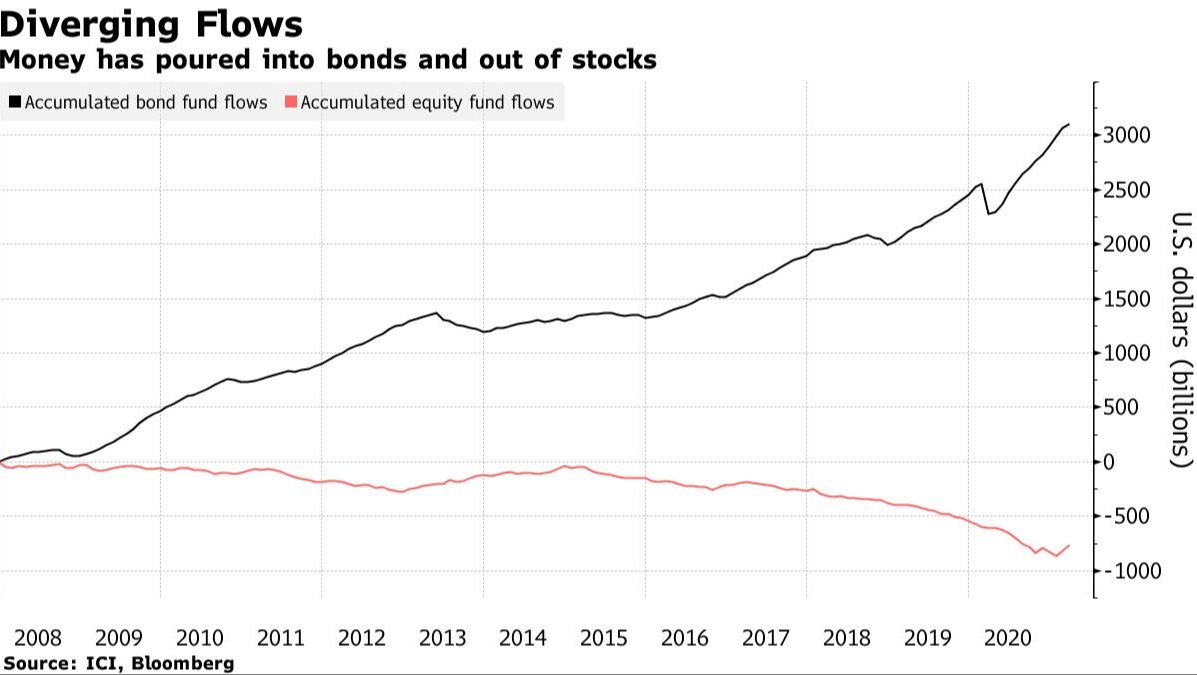

This is certainly a change in investor attitude. From 2008, after the financial crisis, until 2020, equity funds funds lost $800B, while bond funds gathered $3 trillion (T).

CHART 2

However, over the past 5 months, more than $600B has been invested into global equities – exceeding total inflows for the prior 12 years combined, according to Bank of America data. We have argued for quite some time that bonds were unattractive at the very low interest rates which have been and are prevalent in markets today and that stocks, while not “cheap” were and are the only reasonable alternative investment vehicle – especially with a “tailwind” of strong economic growth portending high corporate sales, earnings and cash flows. We still hold this opinion.