Dialing Hong Kong

China has been much in the news of recent. More specifically, President Xi and his pronouncements have captured a lot of newsprint. To many in the markets the regulatory moves over the last several weeks have “smacked” of a return to Maoism. New rules have “dismembered” the for-profit education industry. The tech “tigers” are being brought to heel. Movie stars, who have garnered too much influence in society, have had their internet presence wiped out – literally. The new catch phrase is “common prosperity”. This is the thrust of Xi’s current mantra. Already companies like Alibaba and Tencent have announced programs to share their wealth with the greater society. Over the next several years both corporations will be giving billions of dollars to help those less fortunate – to help spread the common prosperity.

Western investors, large owners of Chinese stocks, have recoiled, fearing that this new, more authoritarian China will not be friendly to or protective of their interests. In a “knee jerk” reaction, Chinese equities have been sold and quite a few pundits have forecasted an “uninvestable” future for China. George Soros, a famed hedge fund investor who years ago “broke” the Bank of England, has declared that recent moves by BlackRock (also a very large and well-respected investment house) to increase its and its clients’ exposure to China a tragedy. The major Chinese stock indexes are down for the year despite good earnings for Chinese companies. The political risk of investing in China right now is considered too great. As a result, some of the best-known Chinese stocks are selling for multiples they have not seen for years. It is “bargain basement” time in Beijing.

Suffering the downdraft in the markets that we have witnessed, we spoke with some friends and “old China hands” in Hong Kong to get their take on the “state of play”. Certainly, nobody at the beginning of 2021 saw this coming. This political interference in the markets has been a “black swan”. So where does it go from here? Quite quickly, our friends reminded us that China practices capitalism with a “Chinese face”. It is not the form of capitalism that is espoused in the U.S. and this must be remembered. According to our contacts, it has been the case and will always be the case that the Chinese Communist Party (CCP) reigns supreme. It is the Communist ideology, reformed by capitalism that produces the Chinese form of capitalism, which holds sway – which controls life in China. Periodically, the CCP feels the need to “discipline” certain swathes of Chinese society for attempting to gain too much influence. Remember Tiananmen and the students who wanted more political power? They were crushed. Pundits then said that China was and would be “uninvestable”. That was in the 1980’s but was certainly not the case after a bit of time passed. Certainly, China will be in “the penalty box” with international investors until they can get more comfortable again with Chinese capitalism. Also, once the CCP has disciplined whom they need to discipline, the regulators will become more friendly, and the markets will respond. The Chinese Economy is too big to ignore, especially in the future. The market opportunities are too big to ignore – especially after this recent “meltdown”. Have international investors seen something like the current political interference in the past? Yes. Has such political interference made China “uninvestable”? For a while – but for the long term, no. Finally, but importantly, the Chinese people have tasted the “fruits” of capitalism. They have witnessed economic success – something they never had with Communism or especially Maoism. President Xi can discipline some wayward citizens, but he cannot go back to China of the 1960’s with the famines and poverty experienced then by the masses. We do not believe the Chinese people will accept that. So, while not racing out to buy a basket of Chinese stocks immediately, we would be collecting names for future investment to try to take advantage of the cheap prices the markets have given us.

Hello Houston

We had written at the end of last year that we thought oil would trade in the markets between $50/barrel and $60/bbl. Oil now trades at more than $70/bbl. Our rationale had been that between $50 – $60/bbl., oil companies make good money. They would also have enough cash flow to pay down debt, something their bankers wanted them to do urgently. Also, that range of prices was not rich enough to tempt oil company managements (or their bankers) to spend capital to drill new wells and thereby expand inventories of crude, creating the potential for another price war. For the oil industry to get out of the recession in which it was because of the low pricing debacle brought on by the OPEC pricing war, it had to remain disciplined with regards to its capital expenditures. It could not, as it had done in the past with their bankers’ blessing, drill beyond free cash flow. So far in 2021, drilling discipline has been maintained.

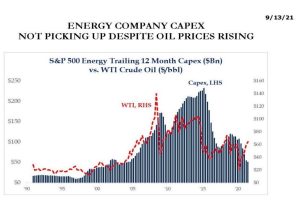

Chart 1

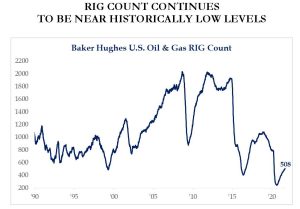

Chart 2

Source: Strategas Securities, LLC – Investment Strategy

As can be seen in Chart 1, oil company capital expenditures have gone down, while the price of oil has increased. Also as illustrated in Chart 2, the number of wells drilled in the U.S. is near an all-time low. This is what was expected. Demand for crude has been generally good, as economies have re-opened, people are traveling more than they did in 2020 and businesses are using more energy than they did in 2020 as they are more active. Also, OPEC+ has been pretty disciplined. The organization has stuck to its production plans in concert with the re-opening of the world, so as not to supply too much oil to recovering economies. So far so good as all the major actors in this play are behaving themselves. It is a bit worrisome for the delicate balance of oil supply and demand when prices get too high, because temptation creeps into the equation. Right now, oil company shareholders are being rewarded with increased dividends and buybacks because of increased oil company cash flows. Oil company bankers are being rewarded with loan payoffs because of increased oil company cash flows. OPEC+ is being rewarded with higher revenues due to higher prices because of overall market production discipline. Everyone is happy. But we think the price of oil is a touch too high and presents temptation. Please remember that OPEC+ still has millions of barrels of daily production which it is artificially holding off the market in support of prices. If OPEC+ decide to open the valves or if the market “got wind” that OPEC+ was thinking about doing so, pricing would fall and perhaps sharply. This is what some oil company managements out of Houston are telling us. Looking a bit further out, assuming current production discipline holds for another year, there will be a real need for more production. As American oil inventories get used up, as U.S. production declines due to the lack of drilling in the U.S. for an extended period of time and as OPEC+ ramps up to full production satisfying world demand for energy, stronger U.S. pricing will happen and will necessitate more drilling in North America. But that is then and not now and might not happen if the oil market “dancers” lose the “beat of the marketplace”, as they did in 2020.

So…

We have had markets around the world which have performed well so far this year. There are issues of concern (think inflation, interest rates, the dollar, China, the price of oil, etc.) – but there always are. Too many pundits want to be the first to call a turn in the markets, saying they have risen too far, too fast. They are always looking “for the sky to fall”. These “prognosticators” have been wrong for years, as markets have gone up with rising corporate earnings and declining interest rates. One day they will be right as even a broken clock is right twice a day – but not yet, not yet.

Predictions for 2021

- Inflation will stay low. Yes – Still believe that the inflation seen so far will dissipate over time.

- Interest rates will remain low. Yes – The Fed is pointing to late 2022 to increase rates. “Don’t Fight the Fed.”

- The dollar will weaken. Yes/No – Depends on investor sentiment regarding risk – Risk On, then $ Down – Risk Off, then $ Up.

- Oil will stay in the pricing range of $50-$60/bbl. No – Above our range due to good demand and supply discipline (See our note above).

- World GNP (Gross National Product) will rebound strongly. Yes

- Corporate Earnings will rebound strongly. Yes

- Investor “risk appetites” will increase. Yes – Earnings doing well, plus bond market is too expensive.

- International equities will outperform U.S. equities. Yes/No – The “seesaw” action continues, but No has the advantage especially with recent China action.

- In the U.S. infrastructure spending will jump. Yes – Getting closer to some major infrastructure investment.

- U.S. stocks will have a good year with some rotation out of “tech darlings” into more economically sensitive names. Yes

A Final Thought