The cost of higher education is a daunting thought for most American families. With the average cost of a public 4-year in-state degree exceeding $156,000 and that of a private university above $223,000, this valuable investment in our children’s futures may seem unattainable.(1) For those of us with children, grandchildren, nieces, nephews, or other loved ones who we would like to help, the 529 Plan is worth considering. This piece will discuss the attributes of these accounts, a recent tax law change that enhances the value of the 529 Plan, and other savings vehicles that could be appropriate for you.

What is a 529 Plan?

The 529 Plan is a tax-advantaged investment account in the United States designed to promote saving for the future higher education expenses of a designated beneficiary. Anyone can contribute to a 529 Plan up to contribution limits, and assets grow tax-free until they are withdrawn for qualified education expenses (tuition, room and board, books, computers, etc.). Because these plans originate at the state level, there are differences in account types and tax benefits by state. Each 529 Plan has an owner and a beneficiary. In most cases, the owner (often a parent or grandparent) starts the 529 Plan for a minor, but it is possible for the owner and beneficiary to be the same person in the case of an adult saving for his or her own higher education. Additionally, most states permit $10,000 per year to be withdrawn from a 529 Plan for private K-12 tuition and associated expenses.

How does one know which account type to choose?

There are two primary types of 529 Plans: savings plans and prepaid plans

- 529 Savings Plans are investment accounts, offered though a state and usually administered through a mutual fund company. Contributions are invested in stocks and bonds with the performance of the 529 Plan tied to the performance of the underlying assets. Assets grow tax-free and the owner of the 529 Plan will have a varying level of control over the investment allocations, depending on the state. Nearly every state offers a 529 Savings Plan. These plans may be best for those with a higher tolerance for volatility in the plan’s market value and for those willing to accept more risk to achieve a higher return.

- 529 Prepaid Plans allow one to purchase tuition credits that appreciate commensurate with the cost of education. As tuition costs rise, these accounts are designed to track the increase, allowing the owner to keep up with inflation regardless of the stock market’s performance. Although these funds are in a pooled investment vehicle, the state sponsored plan accepts the investment risk rather than the college saver. Currently, there are nine states offering this type of plan: Florida, Illinois, Massachusetts, Michigan, Nevada, Pennsylvania, Texas, Virginia, and Washington.(2) These plans are ideal for those wanting to lock in future education costs in today’s dollars.

What are the contribution rules and are my contributions tax deductible?

- Contributions can be made by anyone, not just the account owner. However, some states allow only the owner to receive an income tax deduction on contributed funds.

- 529 Plan contributions are considered gifts, so many will choose to contribute $18,000/year or less to avoid having to report the gift to the IRS. However, larger gifts up to your state’s limit are acceptable.

- The IRS allows for the “superfunding” of a 529 Plan. This means that making up to 5 years of $18,000 contributions at once ($90,000) is permissible, provided that the same individual refrains from contributing for that amount of time.

- Most states, including Pennsylvania, offer a state tax deduction for contributions made to a 529 Plan. Example: A parent superfunds a child’s 529 Plan with $90,000 (5 years of contributions at once). That parent can deduct $90,000 from taxable income on his or her PA state tax return. A joint filing couple could double this amount and deduct $180,000 in one year. Note that most states do require that its own state 529 plan be used for a contribution to be deductible. However, Pennsylvania is one of nine “tax parity states” allowing all 529 Plan contributions, regardless of state, to be deductible. Therefore, residents of Pennsylvania may benefit from considering other state’s plans when initiating a 529 Plan.

What changed in 2023?

Prior to 2023, excess funds in a 529 Plan not used for qualified educational costs were subject to a 10% IRS penalty upon withdrawal. Although most funds grew tax-free for many years, nobody enjoys being penalized, and this was a commonly cited drawback of the 529 Plan. Presently, excess funds in a 529 Plan up to $35,000 can be rolled into a Roth IRA for the beneficiary, without penalty. This can be done over time as the rollover amount for each year is limited to the Roth IRA contribution limit for that year ($7,000 in 2024). Additionally, the account must have been open for 15 years to qualify for this Roth IRA rollover, and funds contributed during the previous 5 years are ineligible. The bottom line is that, although restrictions exist, a 529 Plan that is not fully spent on education can now be moved into a Roth IRA. This allows for continued tax-free growth of the assets, potentially for the beneficiary’s lifetime.

Who should be the owner of the 529 Plan?

In most cases, a parent or close family member will be the owner of the plan. At the time of account opening, the owner and a “successor participant” will be established in addition to the beneficiary. It is important to consider the successor carefully as that person will have broad-based power over the account if the owner passes away or becomes incapacitated. Changing investment allocations, changing beneficiaries, and withdrawing funds fall under the owner’s control.

What other investment vehicles are commonly used to save for a minor?

- Uniform Gifts to Minors (UGMA) and Uniform Transfers to Minors (UTMA) are custodial accounts used to transfer assets to a minor. These transfers are irrevocable; however, the custodian manages the assets and can withdraw from the account for the minor’s benefit. At the age of 18 to 25, varying by state, assets and control of the account must be transferred to the beneficiary. Although these accounts lack the tax benefits of a 529 Plan, they offer flexibility of investment options and are ideal for adults interested in transferring financial assets to a minor while delaying the change of control.

- Educational Savings Plans (ESAs), also known as Coverdell Plans, are offered in thirteen states and are now much less popular than 529 Plans. Contributions are limited to $2,000/year per beneficiary and contributors are subject to relatively strict income limits. Although the investment universe is broader than in a 529 Plan, funds in (ESA) plans must be spent or transferred by age 30.

- Saving in a Roth IRA is another option. With this strategy, parent(s) make contributions to their own Roth IRA while the child is young. When the time comes for higher education, the contributions, not the earnings on those contributions, can be withdrawn tax-free provided that the account has been open for at least 5 years. Should the child not attend college or if the funds are not needed, then the parent continues to own a valuable Roth IRA.

- Trusts are commonly used as a method of transferring assets for the benefit of a minor. Benefits of a Trust include the ability of the grantor(s) to set preferred rules regarding when and how assets can be withdrawn from the Trust. Trusts are often created to continue beyond the lifespan of the original beneficiary, allowing the grantor(s) to create a legacy by supporting future generations. Drawbacks include the costs associated with forming the Trust and annual tax filing requirements.

How to get started?

If you have not yet opened a 529 Plan for a loved one and have interest in doing so, now is the time to get started to ensure that your contributions are able to grow and compound over time. Investing now, even by starting small, in an account that allows for tax-free growth will go a long way in defraying the future financial burden of higher education. Your Baldwin advisor can help you determine which investment vehicle is best for you based on your objectives and where you live. We look forward to hearing from you.

Footnote (1): educationdata.org “Average Cost of College and Tuition” November, 2023

Footnote (2): Investopedia.com “The Last States with Prepaid Tuition Plans” April, 2023

Charts of Interest

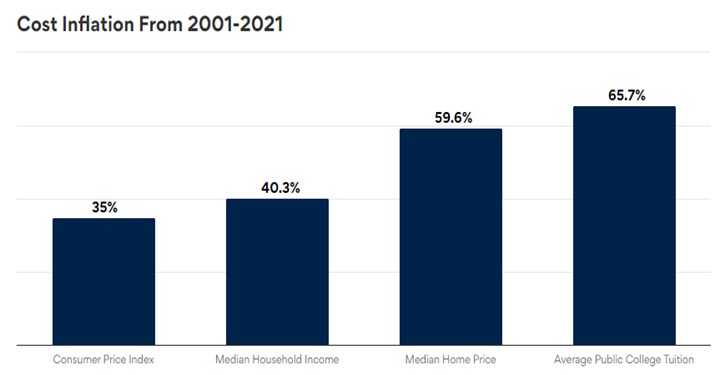

Tuition inflation has outpaced the consumer price index, median household income, and median home prices over the 20-year period ending in 2021.

*Source: NCES, Bureau of Labor Statistics via bestcolleges.com

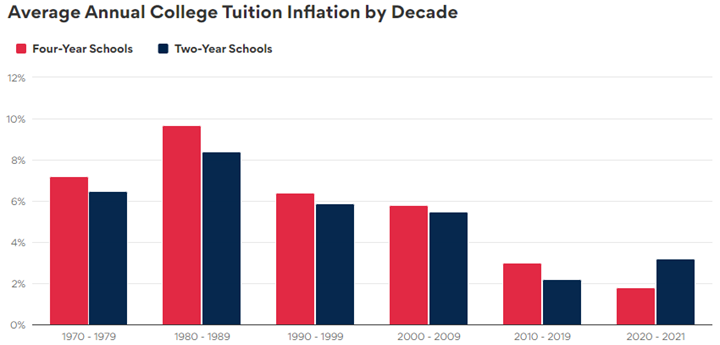

A silver lining is that tuition inflation rates have been disinflating since the 1980s. This is to say that prices are increasing at a slower rate than in the past.

*Source: NCES via bestcolleges.com

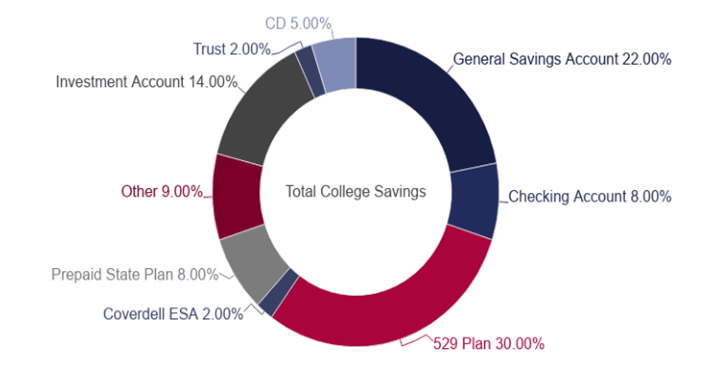

Since its creation in 1996 as part of the Small Business Job Protection Act (a piece of legislation that had little to do with saving for college) the 529 Plan has grown in popularity and now represents the largest percentage of college savings for American families.

*Source: Sallie Mae – How America Saves for College, economicdata.org

Baldwin Management LLC. (“Baldwin”) is a registered investment adviser that does not suggest a certain level of skill or training. The views and opinions expressed in this newsletter are those of Baldwin professionals and may change at any time without prior notification. There is no guarantee that the objectives of any investment program will be achieved. Any strategies or securities discussed is not a recommendation to invest in such strategies or to purchase or sell securities. Investing involves the risk of partial or total loss that investors should be prepared to bear. Past performance is not a guarantee of future results.. The value of investments may be worth more or less than their original cost when sold. Baldwin obtains information from third-party vendors believed to be reliable; however, the accuracy of such information is not guaranteed. For additional information regarding Baldwin’s business practices, registration status and important disclosures, please click on the following link and type our name in the space provided IAPD – Investment Adviser Public Disclosure – Homepage (sec.gov)

Jared V. Quereau, Managing Director

Jared Quereau is a Portfolio Manager and Investment Committee member for Baldwin Investment Management. He has 24 years of industry experience and joined Baldwin in 2020.

Most recently, Jared held the roles of Portfolio Manager and Technology sector analyst at BB&T Securities, the successor firm of the Stratton Management Company. His prior experience includes Equity Trader at Great Point Capital and Registered Representative at Charles Schwab & Company.

Jared earned a B.S. in Finance from the University of Colorado at Boulder and is a member of the CFA Institute and CFA Society of Philadelphia.