Stock market corrections, broadly defined as a drop in price of 10% or more from a recent high, are normal occurrences that long-term investors must accept in exchange for investment returns that outpace inflation over time. Looking back 50 years to 1975, there have been just three years that did not suffer a decline of at least 5% and roughly half of the years saw a decline of 10% or more. Given that the U.S. stock market has always recovered from these events, and often swiftly, it may seem obvious to many of us that doing nothing is the correct course of action. However, market declines are almost always accompanied by a daunting reason not to buy, or something so ominous that some feel the need to consider selling to avoid further losses. In early 2025, it has been the fear of tariffs and a trade war causing an economic slowdown. In 2020, it was the COVID-19 virus causing illness and businesses to shudder. This article will lay out several actions that long-term investors and their advisors can engage in to benefit from these inevitable market declines.

For perspective, let us start by looking at a chart of all major U.S. stock market declines since the 1980’s. Although these were severe in nature and resulted in painful bear markets, we can see that the long-term impact was tolerable for those who remained invested.

Fidelity.com – A Game Plan for Market Corrections – 4/5/2025

Morningstar via Blackrock’s “Navigating retirement savings during volatile markets” – April 2025

#1 – Consider making changes to the amount and timing of your contributions and withdrawals to investment accounts

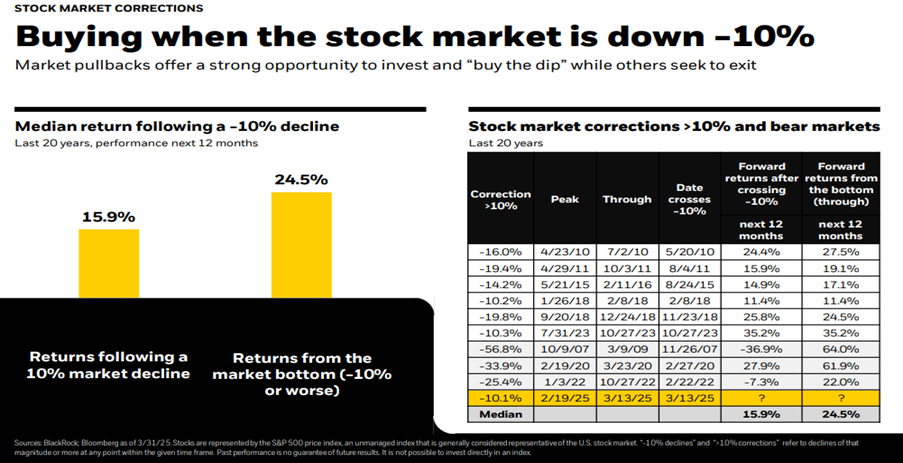

Whether you are at a point in life where you are contributing regularly to a retirement/investment account or taking regular withdrawals from your retirement account, consider opportunistic changes to the timing of your contributions. For example, if you plan to make the maximum contribution to your IRA or 401(k) through equal contributions on a set schedule, accelerating and/or increasing these contributions, starting once a market decline exceeds 10%, can significantly enhance returns over time. Alternatively, if you are in retirement and living on a fixed income through regular withdrawals from a retirement account, you may benefit from temporarily lowering or postponing withdrawals during a correction. Keeping the annual withdrawal rate at 5% or below, especially during down years in the stock market, will help to preserve the balance of your retirement account. Although this strategy may not be possible for everyone due to cash needs, it is worth considering for those who have the flexibility to make these adjustments. The following table depicts the future returns generated by the S&P 500 from the day that a 10% correction occurred, as well as what would have been gained from the low point of each correction.

Blackrock: Student of the Market – April 2025

#2 – Consider Roth IRA Conversions

A “Roth Conversion” refers to the process of transferring funds from a traditional IRA or 401(k) into a Roth IRA. Since this conversion involves moving pre-tax dollars into a Roth IRA that may contain only after-tax dollars, the conversion is a taxable event in the year that the monies are converted. For example, John Doe decides to convert 25% of his Traditional IRA into his Roth IRA in 2025. The dollar value of that conversion, whether it is held in cash or investments, will show up on his year-end tax form as ordinary income (just like wages) for that year. The taxable amount is marked to the value of the assets at the time of conversion. Therefore, it makes sense to strategically execute these conversions when asset prices are down, allowing the assets to grow back from depressed levels while inside the tax-advantaged Roth IRA. Whether or not to do a Roth Conversion is an individual decision that depends on one’s age, expected tax bracket, and sensitivity to paying taxes now vs. later in life. Although this process can be of value to almost anyone, younger investors and recent retirees without substantial other income are ideal candidates to consider converting funds during stock market downturns.

Here is a final example to illustrate the point: Jane Doe is a successful real estate agent whose income puts her in the highest tax bracket most years. She has consistently made the maximum allowable contribution to her Traditional IRA and has seen its value grow over the years. Unfortunately, there is a sudden economic slowdown that causes the stock market to tumble. In addition, the real estate market softens, and her income is now expected to be far lower than normal. By December, she can see that her total income will be a fraction of what she typically earns. She opportunistically decides to convert a portion of her Traditional IRA into a Roth IRA, being careful to make sure that her taxable income for the year stays just below the level at which each additional dollar would be taxed at a higher level. Rather than panicking during a stressful time, she has acted proactively to bolster the long-term growth of her retirement assets.

#3 – Tax-Loss Harvesting

Tax loss harvesting, also known as realizing losses, involves selling securities held in your taxable accounts that have declined in value from your purchase price. During stock market corrections, investors can meaningfully lower their future tax payments by realizing losses and simultaneously switching into a similar, but not identical, security. For example, let’s assume that Investor A invests $100,000 into a large-cap-growth mutual fund in November of 2024. By March of the following year, the value of the investment falls to $75,000 amid a stock market correction that hits growth-oriented stocks particularly hard. Rather than waiting for a recovery, Investor A chooses to sell the shares at a loss, immediately reinvesting the proceeds into a different fund that closely tracks the performance of large-cap-growth stocks. Later that year, the stock market recovers its losses and Investor A’s investment returns to breakeven. Because of this tax-loss harvesting strategy, this investor has a $25,000 realized capital loss that can be used to offset realized capital gains, into perpetuity. Additionally, if there are no capital gains to offset, $3,000 per year of this loss can be deducted against ordinary income. Many investors overlook this strategy due to how unappealing it is to sell an investment at a loss during a period of market stress. For some, this is akin to admitting defeat or “throwing in the towel” with the risk of having sold at a low point. In the end, it is an investor’s net return after all taxes and fees that truly matters. A dollar saved in capital gains tax is equally valuable to a dollar earned in an investment. So, when looking at the situation from this perspective, anything we can do to enhance that return by lowering a future tax obligation is worth considering. At Baldwin, our portfolio management involves sensible tax-loss harvesting to ensure that our clients are not paying more capital gains tax than necessary.

These strategies can be valuable tools to help use stock market corrections to your financial advantage. Additionally, it satisfies the common urge to “do something” during a period of market stress. Rather than this action being an emotional decision that will likely result in a long-term setback to meeting your financial goals, the strategies laid out above will have a positive impact if done carefully. Your Baldwin advisor is aware of these strategies and can assist in their implementation.

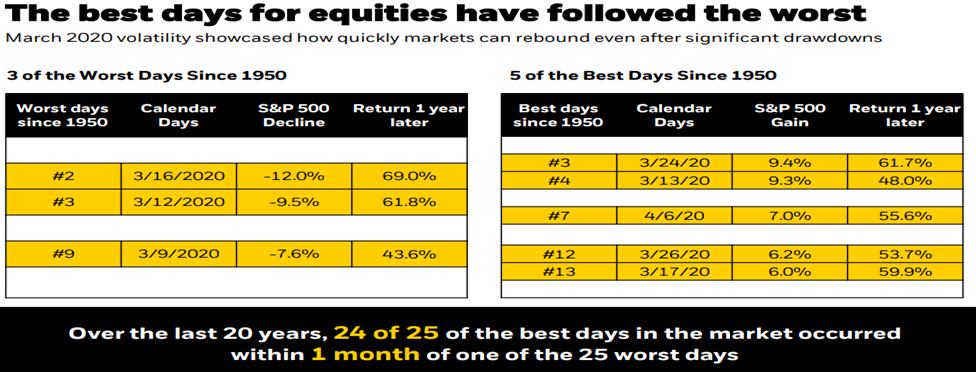

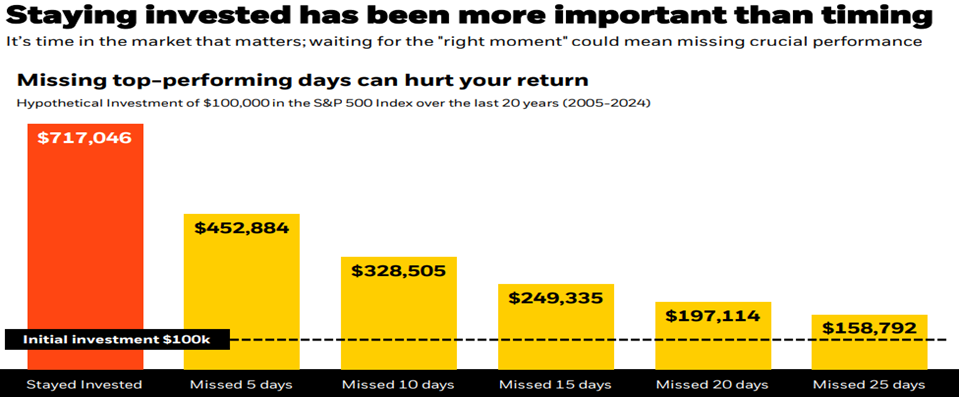

In conclusion, several charts are included below which provide some historical perspective on stock market volatility and the benefits of remaining invested through difficult times.

Source: Blackrock: Student of the Market – April 2025

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosure.

Jared V. Quereau, Managing Director

Jared Quereau is a Portfolio Manager and Investment Committee member for Baldwin Investment Management. He has 25 years of industry experience and joined Baldwin in 2020. Most recently, Jared held the roles of Portfolio Manager and Technology sector analyst at BB&T Securities, the successor firm of the Stratton Management Company. His prior experience includes Equity Trader at Great Point Capital and Registered Representative at Charles Schwab & Company. Jared earned a B.S. in Finance from the University of Colorado at Boulder and is a member of the CFA Institute and CFA Society of Philadelphia.