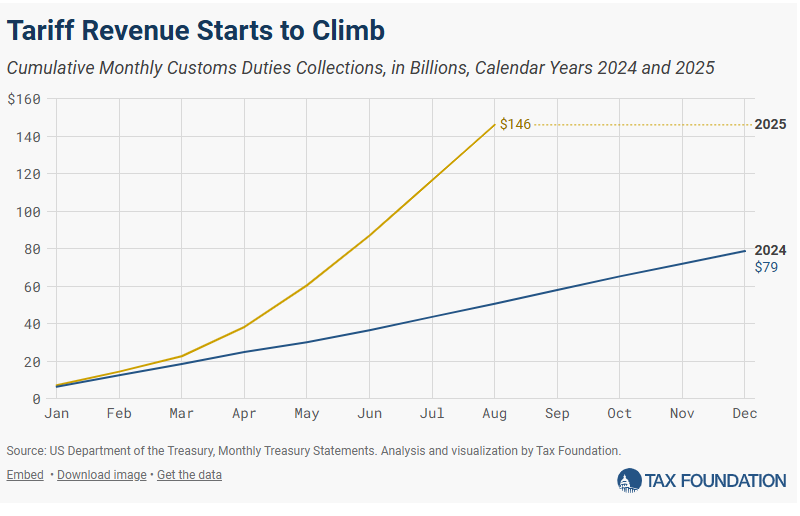

We’ve now had several months of experience with the newly imposed tariffs since Liberation Day, April 2, 2025. The experience has not been consistent because there have been exceptions and delays, which have created their own set of frustrations for business – but the application of tariffs on various imported products has started even after frameworks for trade deals have been negotiated. It was once thought that after negotiating a deal with an exporting country to the US that if all foreign duties on a product were eliminated then there would be no corresponding American duty. This is no longer the case. It seems that the US will impose a duty regardless of any similar foreign tax elimination. So far, the US government has raised a good bit of money, as can be seen in Chart 1 below.

CHART 1

According to Yale’s The Budget Lab, “The average effective tariff was 10% in June and likely about 10% and 11.5% in July and August, respectively, versus 2.4% at the beginning of the year”. So costs have appreciated smartly.

Who has been paying those increased costs so far? There are three parties, broadly speaking, in any transaction involving the purchase of an imported good: the exporter, the importer and the ultimate consumer. Technically, it is the importer who pays the tariff when the good arrives onshore in the US and the importer takes possession. To offset at least a part of the increased cost of the product due to the tariff, a large importer could renegotiate (i.e., lower the price) in order to get the exporter to share some of the increased cost. Only a large importer would have the market share strength to successfully renegotiate prices with an exporter. The importer also could shave profit margins to absorb part of the tariff. This would be uncomfortable for the importer – but for strategic business purposes, an importer might suffer shrinking profit margins for a time to avoid losing customers. That time will not be forever. Finally, consumers might/will have to bear the burden of higher prices for a product they want (and that has no reasonable substitute) as importers pass along costs – just as historical experience guides us. Since Liberation Day, it has been the position from Washington that it would be the exporting countries which would pay and have been paying the tariffs imposed. Unfortunately, that has not been experience so far.

“Foreign exporters had absorbed 14% of the cost of all tariffs implemented so far through June, but that their share will rise to 25% if the more recent tariffs follow the same pattern as the earliest tariffs on China. … US consumers had absorbed 22% of tariff costs through June but that their share will rise to 67% if the recent tariffs follow the same pattern as the earliest ones. This implies that US businesses have absorbed more than half of the tariff costs so far but that their share will fall to less than 10%” wrote the analysts – Goldman Sachs, August 10 note to clients

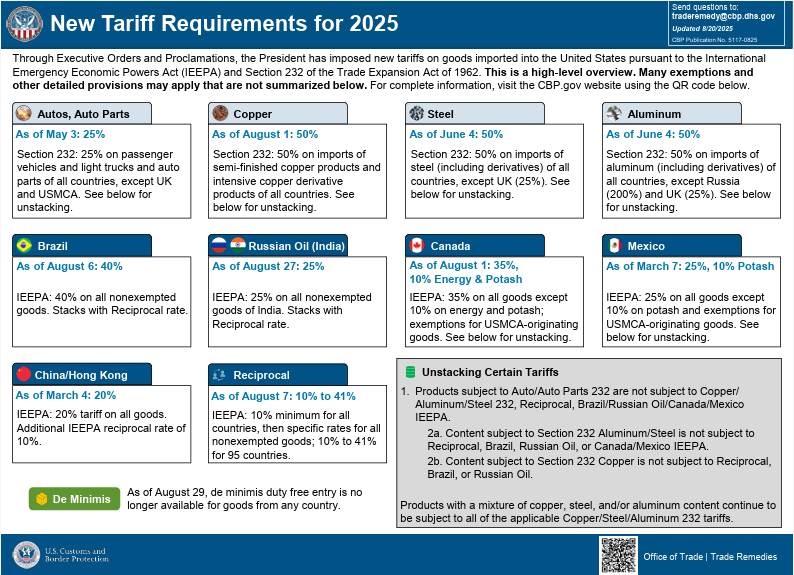

The increased costs connected with tariffs are not just the higher “sticker price” when an importer takes possession of an imported good. There has also been (and will be as long as tariffs survive) increased red tape costs. The ever-changing (at least so far) trade rules are adding hours of extra work for companies trying to follow the new trade rules, as can be seen below.

CHART 2

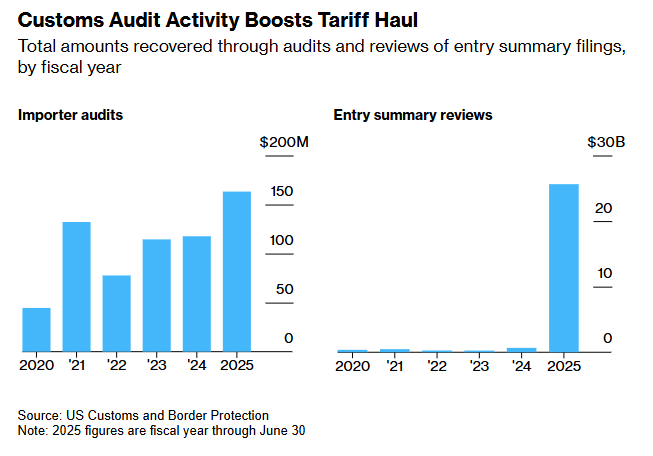

For example, if an importer cannot prove the origin of some imported aluminum, customs officials will assume the metal came from Russia, which is charged the highest import duty of 200%. According to Hugo Pakula, CEO of Tru Identity, an AI automation platform for global trade, the importation of a simple product would require “…at least one to three hours of work on the low end, while more complex cases – like figuring out the metal content in a shipment of motorbike parts – could take 10 hours or more”. Importers must be able to document not just the value of the metals contained in the goods, but also where the metal was poured and the aluminum was smelted. As can be seen in Chart 3, customs audit activity has grown dramatically – increasing costs.

CHART 3

Compliance costs burden any business – but fall particularly hard on small companies. A large firm can better absorb added regulatory expenses. A small corporation cannot. A large company can pivot, adjust, absorb or force an exporter to share more of any cost burden. A small company does not have such flexibility and will thus feel more of the tariff pain.

In any event, how is corporate America holding up? So far, the report from at least public companies is that US businesses generally are handling tariffs well. The headline duties printed in newspapers are not usually the tariffs that get implemented. There are exceptions, and there have been delays resulting in an actual tariff lower than the advertised one. Further, large companies have been able to adjust supply chains to some extent, altering logistics routes to change products’ ports of embarkation and thus alter the duty imposed when the product finally changes hands in the US. Also, within any large company there are always levers to pull to move various costs around the corporate income statement. Company efficiency is newly found. Lastly, there are companies (like Best Buy, Home Depot, Macy’s, Mattel and Nike) which have announced that prices on certain items will be rising to cover the cost of tariffs and protect company margins. As a result, through the first six months of 2025, corporate sales, earnings and cash flows have pleasantly surprised Wall Street analysts. The vast majority of company reports have been better than Street expectations, further supporting stock price valuations. At the start of the second quarter, corporate earnings were forecasted to rise approximately 4% year over year. Instead, company earnings increased some 12%. While a number of pundits think that equity valuations are stretched, this kind of business performance, which has been repeated over the last few years, continues to underpin seemingly high valuations.

Also, with evidence clearly suggesting that it has been and will be the American consumer who will bear the lion’s share of the import duties extant, how is the American consumer faring? We have written in the past on several occasions that the American consumer represents about 70% of US GDP (Gross Domestic Product). The American shopper is the “backbone” of the US economy. So, if America is to move forward, it will be up to the American consumer to provide the economic fuel. To gain recent insight on the condition of the US consumer, we gathered research from Liz Evertt Krisberg, head of the Bank of America Institute and Deputy Director of Bank of America (BofA) Global Research, as outlined in Barron’s (September 8, 2025). The Institute’s research database is comprised of 70 million BofA individual and business customers, $1.3 trillion in deposits and $4 trillion of annual transactions conducted through BofA. According to Liz, “at the Institute, we are sharing not what people tell you, but what 70 million people are doing”. Currently, BofA would characterize the American consumer as resilient and agile. For lower income consumers, the strength of the labor market and earnings have bolstered resilience. For higher income consumers, stock market and real estate gains have been supportive. Total debt payments to disposable income have been falling and are below historical averages. Higher income consumers are driving more than half of US economic growth and spending, middle income consumers garner a 30% share and the lowest third have a 15% share. Interestingly, the proportion of all households paying off their credit card balances in full is higher today than in 2019, and the share of households carrying a balance on their credit card is lower. Further, the ratio of credit card balances to monthly income is less than in 2019, and people have more money in their checking and savings accounts. So, as we have reported in the past several years, the American consumer seems to be well positioned to take on America’s new tariffs. There has been and probably will be continued griping about higher prices – but the American shopper remains resilient and will, although not gladly, pick up the check.

To recap, exporters to the US will likely continue to pay a minor share of American duties via lower product prices to help their customers. American importers, now bearing the largest proportion of the new tariffs, will do so only for a finite period of time. Company profit margins will get nicked – but there are levers which have been used and will be used to largely protect margins. Eventually, most of the tariff costs will be passed along to the ultimate consumer. A tariff is a consumption tax. A tariff is a sales tax. The entity which has benefited the most from this duty exercise is the US Federal government, which has seen its coffers swell by tens of billions of dollars – so much so that S&P Global Ratings recently affirmed its stable outlook on US Treasury debt, noting that tariff collections were expected to help offset weaker revenue from recent fiscal legislation, specifically the recently passed tax bill. In that bill, most of the legislation made permanent individual tax brackets which were about to expire. Only a few individual taxes were cut. The recently imposed tariffs put a new sales tax on many items American purchase every day. In short, there was an exchange of an income tax for a consumption tax.

Economic Chart Checks……

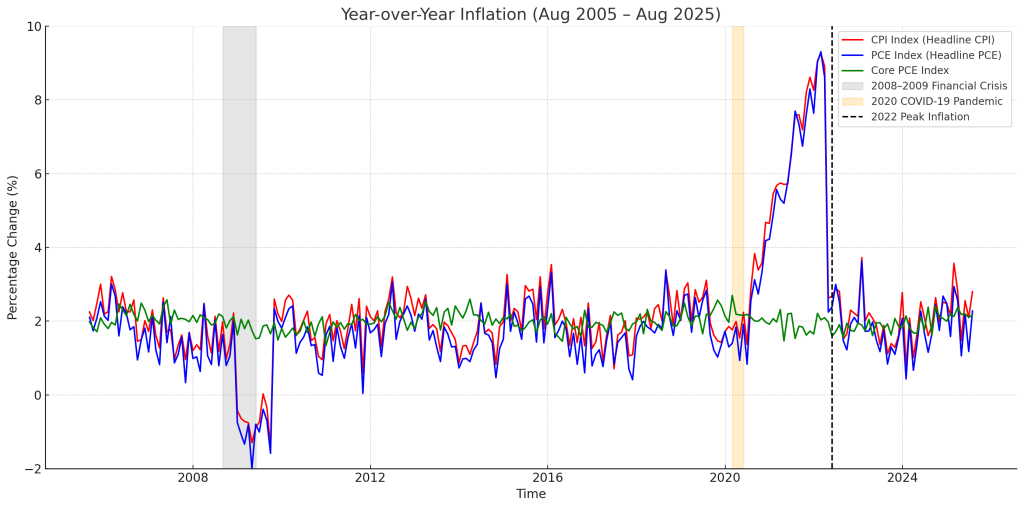

In Chart 4 below, inflation so far seems well controlled. While not yet at the Fed’s 2% goal, it is close and tending to go lower according to the most recent figures.

CHART 4

The relatively good behavior of inflation has now allowed monetary authorities to focus on its other major mandate, low unemployment. As can be seen in Chart 5 following, unemployment is near historically low levels. But recent numbers, including adjustments to past employment figures, have demonstrated softer employment than earlier thought and a slight increase in unemployment.

CHART 5

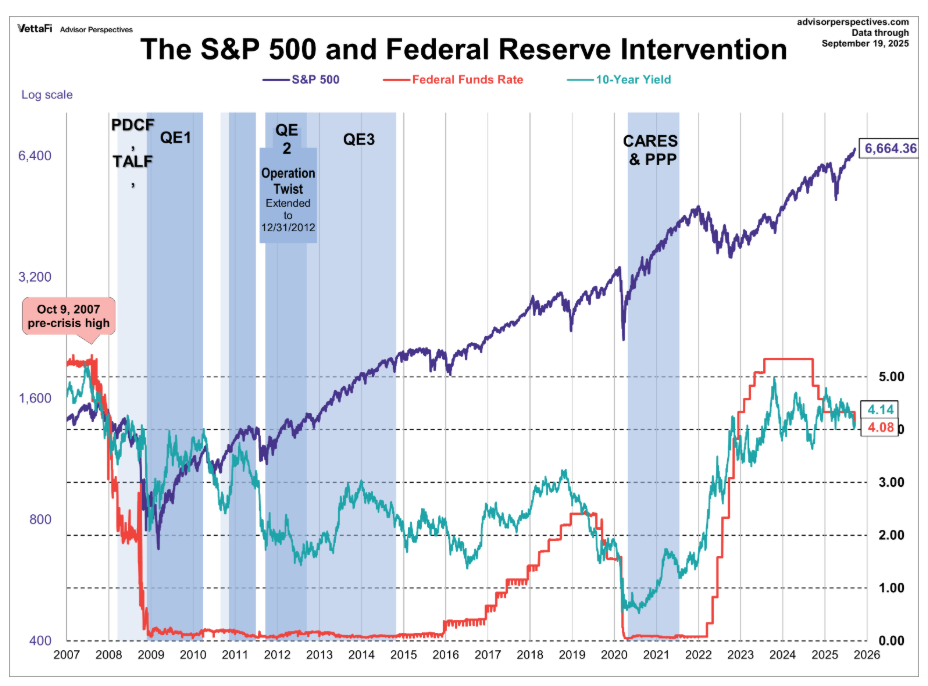

This most recent data have pushed the Fed to cut interest rates for the first time in 2025 – along with expectations that the Fed will continue to cut rates for the rest of this year. Finally in Chart 6, the reader will note the fall in interest rates aforementioned – as represented by the Fed Funds rate and the 10-year Treasury yield.

CHART 6

Falling interest rates have been and should be supportive of the stock market.

A FINAL THOUGHT….

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosure.

Peter H. Havens, Chairman of the Board, Investment Portfolio Manager

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.