“Priced In” – How Expectations Shape Investment Returns

If you’ve ever been puzzled by watching the stock market decline on what seemed like good news, or rally when a headline looked terrible, you’re not alone. It is one of the most common sources of confusion and frustration among investors, and it strikes at the heart of how financial markets work. The stock market is more than just a scoreboard. It does not simply reflect what has happened; it reflects what investors and traders collectively expect to happen. This distinction, between outcomes and expectations, is an important concept in investing. Understanding and accepting it can mean the difference between reacting emotionally to short-term noise and maintaining the discipline required to build long-term wealth.

The Market Is a Discounting Machine

At any given moment, the price of a stock, or an entire index like the S&P 500, represents the aggregated wisdom of millions of participants, each expressing an opinion as to what the future holds. Earnings growth, interest rates, economic data, geopolitical risk, and all other available information are baked into the equilibrium price of each transaction between a buyer and a seller. This is what is meant when financial markets are referred to as “discounting mechanisms.” They anticipate news rather than waiting for it to arrive, which is why what matters most to markets is whether the outcome was better or worse than what was expected. In most cases, stock prices have already adjusted before the average investor has a chance to capitalize on news.

The Power of a Surprise

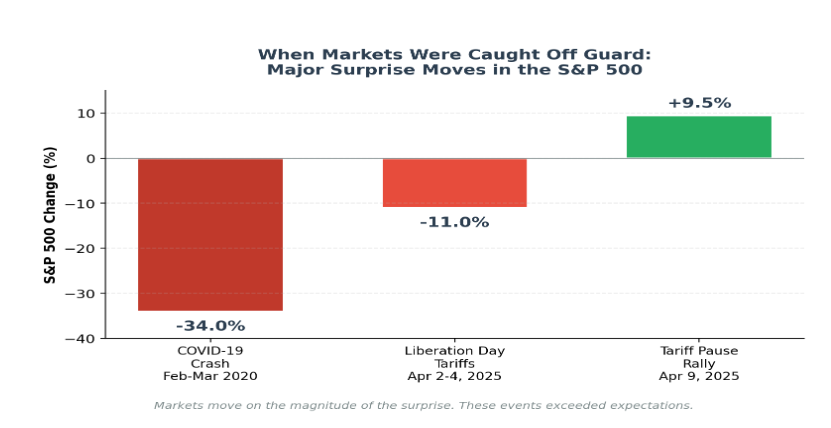

This is why the biggest stock market moves are almost always triggered by surprises, events that deviate significantly from the consensus expectation. The COVID crash of 2020 remains one of the most dramatic examples in recent years. During February and March of that year, the S&P 500 shed over one third of its value as the pandemic spread. Obviously, nobody had priced in a global pandemic shutting down the world economy virtually overnight. The surprise was enormous, and the market’s reaction was proportional.

However, just five months later, the S&P 500 recovered the entire loss, returning to its pre-crash highs. The market had begun pricing in the recovery well before evidence of it had materialized. How could the stock market rise as the pandemic continued to spread, with no end in sight? Fiscal stimulus, Federal Reserve intervention, and vaccine progress gave some investors reason to look beyond the immediate devastation and position for a rebound. Those who panicked and sold at the bottom missed one of the fastest recoveries in history.

We saw this dynamic play out again last April. Heading into the “Liberation Day” tariff announcement, markets had already anticipated a 10% increase in trade barriers. What investors got was far more aggressive: a broad-based tariff increase of nearly 20%, with rates on Chinese goods escalating to astronomical levels. As a result, panic selling set in, sending the S&P 500 down 11% in just two days.

Then came the reversal. On April 9, when a 90-day tariff pause was announced, the S&P 500 surged 9.5%, its best single-day advance since 2008. Markets had braced for further escalation, but the news proved benign. By early summer, the S&P 500 had fully recovered and was setting new all-time highs.

More recently, the rapid advancement of artificial intelligence has provided yet another example. In January, the unexpected release of a powerful AI tool called “Claude Code” triggered a sharp sell-off in many prominent software stocks, as investors suddenly confronted the possibility that AI could replace many of the software subscriptions and services that we rely upon. The S&P Software Index fell 15% in January alone, its worst month in nearly two decades. The full extent of the disruption to traditional software subscription models is not yet known, but the market’s swift repricing reflects a familiar pattern: when expectations are upended by something investors had not fully anticipated, the reaction can be dramatic.

Events like the COVID pandemic, the “Liberation Day” tariffs, and the AI-driven software sell-off are sometimes referred to as “black swans,” a term coined by author Nassim Taleb to describe low-probability, high-impact events that are virtually impossible to predict. By their nature, black swan events cannot be priced in, which is why they produce the most volatile market reactions.

When “Beating the Street” Isn’t Enough

This expectations framework plays out at the individual stock level every earnings season. It is here where investors encounter one of their most frustrating experiences: watching a company deliver strong results, only to see its stock go nowhere, or worse yet, decline.

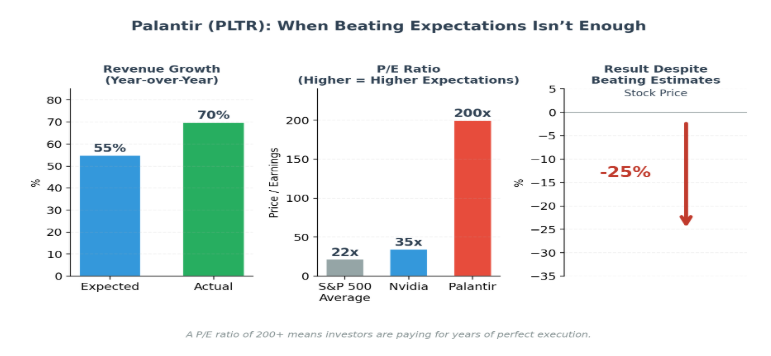

One of the clearest ways to gauge the level of expectation that is already embedded in a stock price is through its price-to-earnings (P/E) ratio, a widely used valuation metric in investing. The S&P 500 Index historically trades at roughly 17–21 times its annual earnings, depending on the economic cycle and sentiment. When an individual stock commands a significantly higher multiple of its earnings, investors are showing a willingness to pay a premium for its expected future growth. As a rule of thumb, the higher the P/E, the higher the bar a company must clear to justify its current stock price.

Let’s consider the case of Palantir Technologies (PLTR), a fast-growing AI-powered software company. Palantir was one of the top-performing stocks in 2025 with its share price rising 130%. The company reported spectacular quarterly results in February, with revenue surging 70% year-over-year and beating analyst estimates handily. Despite this stellar report, the stock dropped 25% in its wake. With a P/E ratio nearly ten times the market average, investors weren’t just expecting a good quarter; they were expecting perfection into perpetuity. A strong beat simply wasn’t enough to justify what was already priced in. In the short term, expectations for Palantir had been stretched too far to keep the stock price aloft.

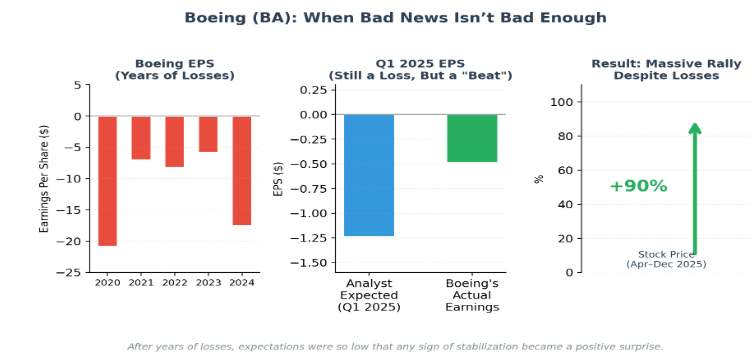

If sky-high expectations can doom a great earnings report, the opposite can also occur. Boeing (BA) provides a compelling example. Entering 2025, the company had not posted an annual profit in five years. Ongoing quality control problems led to steep financial losses and some customers lost faith in the safety of the product. Understandably, expectations were firmly anchored to continued losses.

Then results started coming in less bad than feared. In the first quarter of 2025, Boeing reported a much narrower loss than Wall Street analysts had anticipated, and management signaled a credible path back to profitability. The report was objectively poor and uninspiring, as the company was still losing money, but relative to the bleak expectations already priced in, it represented a positive surprise. The stock subsequently rallied approximately 90% to finish 2025 on a high note for its long-suffering shareholders.

Taken together, these two examples illustrate the same principle from opposite directions. The price you pay for a stock is itself an expression of expectations, and the valuation tells you how high the bar has been set. A great company at an excessive price can still disappoint, while a struggling company can rally on the mere prospect of stabilization.

To be clear, these examples are not an invitation to habitually bet against the most successful stocks, or vice versa. The market’s collective judgement often proves remarkably accurate in its ability to discern what should be expensive and what should be cheap. The point is not that the market was wrong in the examples cited above, but that we see the greatest volatility when a deeply rooted expectation is challenged.

Why This Matters for Your Portfolio

Understanding expectations leads to a critical insight for long-term investors to understand. Trying to time the market around major events is extraordinarily difficult. To trade successfully around an event, you need to correctly predict not only what will happen, but also what the market has already priced in. Even a correct prediction can be unprofitable unless both forecasts are correct. The logical conclusion is clear. A disciplined, long-term investment approach will serve you far better than trying to outguess the market. An investor who stayed fully invested through both the COVID crash of 2020 and the tariff turmoil of 2025 would have seen the S&P 500 deliver an annualized return north of 20%, despite enduring two of the sharpest price corrections in recent history.

In our view, the investors who fared worst over this period weren’t necessarily those who made the wrong prediction. They were the ones who abandoned their strategy in the heat of the moment, leading them to transact at inopportune times. So, the next time you see a headline that tempts you to make an impulsive change to your investments, it is worth pausing to ask yourself: Is this a surprise to the market, or is it already reflected in prices? The real edge in investing isn’t predicting the next surprise. It’s having a plan that is built to absorb surprises, both good and bad, without derailing your long-term goals. Markets will always react to the unexpected and there will be black swan events in the future. The question is whether your portfolio and your temperament are prepared for it.

At Baldwin, we are focused on managing your portfolio with these principles in mind. Our investment team carefully evaluates valuations, assesses what expectations are already embedded in prices, and positions your investments in a way that we believe to be beneficial, so that you don’t have to navigate these dynamics alone. As always, we invite you to contact your Baldwin advisor to discuss your investments.

*The charts in this article were created with the assistance of Anthropic’s Claude AI Assistant and are intended for illustrative purposes only. Data contained within the charts in this article was sourced from S&P Global statistical data, a verified third-party source. AI tools were used solely for graphical formatting assistance.

All references to S&P 500 returns and the return of the S&P Software Index are for illustrative purposes and do not imply that Baldwin clients participated during those periods. The securities identified are for illustrative purposes only and do not represent all securities purchased, sold, or recommended. It should not be assumed that investment in the securities identified was or will be profitable. No actual investor participation in the specific securities referenced is implied.

“This commentary is provided for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. All investments involve risk, including possible loss of principal. Index performance is shown for illustrative purposes only, is unmanaged, and does not reflect fees or expenses. Past performance does not guarantee future results. Securities referenced are for illustrative purposes only and are not to be taken as recommendations. Views expressed are as of the date published and are subject to change without notice.”

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosure.

Jared V. Quereau, Managing Director

Jared Quereau is a Portfolio Manager and Investment Committee member for Baldwin Investment Management. He has 26 years of industry experience and joined Baldwin in 2020. Most recently, Jared held the roles of Portfolio Manager and Technology sector analyst at BB&T Securities, the successor firm of the Stratton Management Company. His prior experience includes Equity Trader at Great Point Capital and Registered Representative at Charles Schwab & Company. Jared earned a B.S. in Finance from the University of Colorado at Boulder and is a member of the CFA Institute and CFA Society of Philadelphia.