Before examining the subject of this commentary, let’s first do a health check on the American economy and the state of its bond, stock and currency markets. Our perspective of the measures at which we will look is that of the market, not of a pundit. At this important time, we want to understand what the markets and their millions of participants are telling us to get as accurate a read as possible on the present situation and the near future.

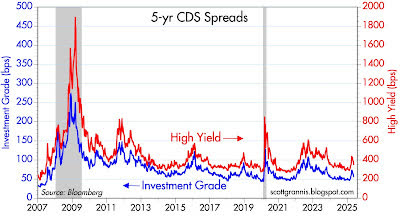

Our first chart examines 5-year credit default swaps spreads. This measures the difference in rates demanded by investors who invest in high yield (aka junk) bonds and those who invest in investment grade bonds. The wider the spread (i.e., the greater the difference), the more nervous investors are about the condition of the US economy. The narrower the spread, the more relaxed investors are about the economic outlook.

CHART 1

As can be seen in Chart 1, spreads are modestly elevated, and we would conclude that the bond market is reasonably confident in the outlook for the economy and corporate profits.

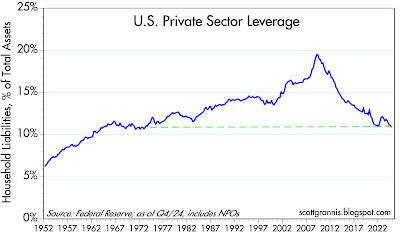

In Chart 2 below, this is a picture of the state of the US private sector (i.e., the American consumer). It is the ratio of total household liabilities to total household assets:

CHART 2

As can be seen, US households are under-levered – which makes the US economy quite resilient because the American consumer represents about 70% of US GDP (gross domestic product). Unfortunately, the same cannot be said about the US federal government, a topic of widespread discussion today.

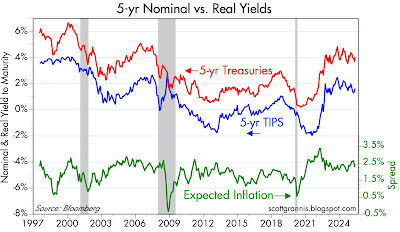

Let’s take a look at another spread relationship in the bond market – the spread between 5-year Treasuries and 5-year TIPS (Treasury Inflation-Protected Securities). This delta represents the market’s implied expectation for the average annual inflation rate over the next 5 years:

CHART 3

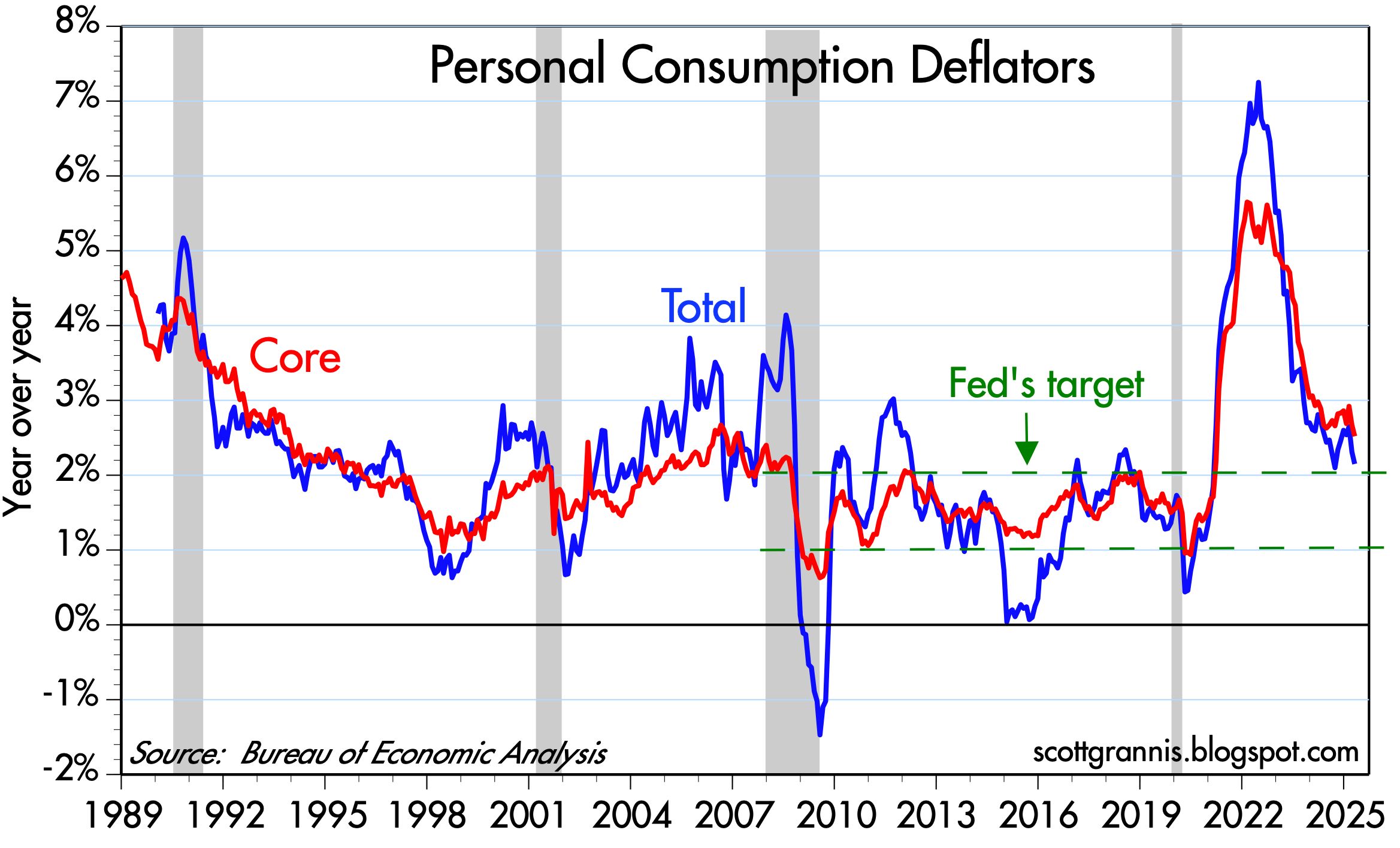

As can be seen by the green line in the above chart, inflation expectations are fairly stable and very close to the Fed’s target of 2%. Achieving that 2% goal would allow the Fed to continue to cut interest rates, which would support both the bond market and the stock market. Another look at inflation is captured in Chart 4 below. This looks at the Fed’s preferred measure of inflation – the Personal Consumption Deflators – both the Total (which includes food and energy measures) and the Core (which excludes the volatile food and energy measures).

CHART 4

Again, the reader will note how inflation has declined dramatically and sits just above the Fed’s target. This is good news and supports why the markets currently are relaxed about inflation as depicted in Chart 3.

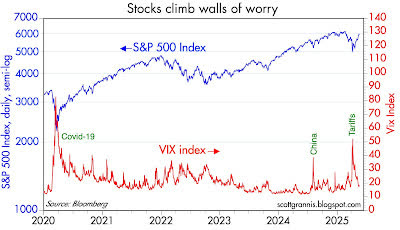

But while the bond and stock markets have not moved a great deal year to date, that does not mean that there has not been a fair amount of volatility throughout the period, especially in the equity markets. Following is a picture of the volatility in the stock market since 2020.

CHART 5

Volatility in this chart is represented by the VIX Index, commonly known as the “fear” index. Note the spike in 2025 with the introduction of tariffs and then note that as the tariffs are delayed, the VIX Index declines sharply, and the S&P 500 rallies strongly. Stocks do “climb a wall of worry” as the old Wall Street saying goes.

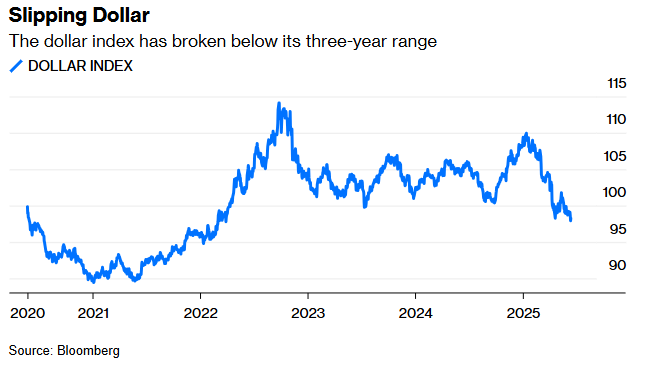

Let’s now direct our attention to some “Known Unknowns” unnerving investors. What we mean here is that we are aware of the concerns or problems. We also know that there will be a result. What we don’t know is the result. This is a Known Unknown. Investors have opinions about what they think the results might be – but nobody knows for certain, and it is the uncertainty attached to the problem that is unnerving investors. For example, investors know that the US has been running huge national deficits annually for a long time. The American budget has not been balanced since the Clinton administration and the deficit has been growing. Further, the US federal government’s balance sheet has deteriorated markedly because of the long-running deficits. The American debt balance is slated to eclipse US GDP shortly and Moody’s, the last major bond rating agency to do so, just lowered the credit rating of US Treasury debt below AAA. The world’s issuer of the world’s reserve currency, America, is no longer triple A credit. So, investors know the problem (spending profligacy leading to annual deficits damaging the federal balance sheet). But what will the result be? Investors do not know – but some “tea leaves” are being read as indicators are becoming apparent and investors are a bit unnerved. Already we have seen the dollar depreciate by approximately 10% in 2025.

CHART 6

Further, plans to cut taxes and raise the federal debt ceiling with insufficient plans to cut spending raise worries about deficits further into the future, compounding an already big problem, as perceived by investors.

Layered on top is the use of the dollar in sanctions against Russia. To punish Russia for its invasion of Ukraine, Russia was banned from using SWIFT – an international messaging network that facilitates secure and standardized international financial transactions. This is the system that enables the transfer of information needed for international payments. The US dollar represents just over half of all foreign exchange traffic sent through the network, significantly higher than the Euro’s share of 21.6%. Not being able to use SWIFT has meant that Russia has had to establish other channels to conduct trade. These other avenues, being outside the normal trade channels commonly used worldwide, has essentially shut down Russia’s ability to trade around the world – severely damaging its economy. Politicizing the dollar by banning Russia’s use of SWIFT makes others wonder if their holdings of dollars are safe.

Tariffs, a not often used instrument of trade policy because they are considered by many to be too blunt, are the focal strategy of American trade and economic relations today. Not only are tariffs being used with abandon, as just about the whole world has been tariffed, but the size of tariff rates is beyond the scope of what has been rarely used in recent history (i.e., triple digit tariffs) and the inconsistency of their use (i.e., announced then delayed due to negative market reaction, then perhaps re-announced and then modified or delayed again) has been confusing for investors, CEO’s, corporate planners, supply chain managers, etc. For too many company heads, it has become too difficult to plan in the current US business environment. So, there is not one business plan or strategy. Instead, there is scenario planning which derives multiple plans because of the lack of clarity. All the above have created uncertainty, and this confusion has unnerved investors.

We noted above that the US dollar has already lost approximately 10% of its value in 2025. While we have not seen the same degree of negative reaction by investors in the American stock and bond markets, we should not ignore the loss in the currency market because much of the US government’s annual financing of budget deficits comes from foreign creditors. It might be too tall of an order to expect foreign investors to buy US Treasuries in the face of a weak dollar. American exceptionalism is being tested and questioned. Investors around the world are making decisions to redeploy assets outside of the US. So, the first asset sold is the US dollar. They are not giving up on the US – but we do not think they will easily return to the same level of concentration of their assets in the American dollar. Year to date, other currencies like the Euro, the Taiwan dollar and the Yen have outperformed the greenback. This US dollar underperformance can have a very meaningful effect on foreign company financial performance if they have invested in the US and are unhedged vs. the US dollar. For example, Taiwan life insurance companies posted a $620 million loss in April as they were unhedged vs. their dollar investments after the Taiwan dollar appreciated abruptly – with speculation that as part of tariff negotiations the Taiwan central bank was encouraged to allow the Taiwan dollar to appreciate against the US dollar. Further, it is estimated by Goldman Sachs, a preeminent American investment bank, that if the Taiwan dollar appreciated 10%, it could lead to a $18 billion unrealized currency loss for Taiwanese insurers, wiping out capital reserves. For years, what was a sure bet – that the US was exceptional, that US stocks only appreciated in value and that the dollar would only be strong – is not so sure anymore. International stock markets have also greatly outperformed the S&P 500 with the MSCI All Country World Index ex USA +13.9% year to date and the S&P 500 +1.7%, as of mid-June 2025. Greater risk has been added to the equation that to solve for greater returns, one need only to invest in dollar-based investments.

We are not suggesting that it is time to hang the black crepe. The US has not fallen from its perch – yet. The American economy has been quite resilient, surprising many pundits. America may no longer be AAA credit, but it is AA credit which is not junk. The consumer is in good shape financially; inflation is still heading in the right direction according to the most recent numbers (although there are worries). Corporate America reported strong first quarter earnings, and most management teams expressed optimism (tempered with some confusion about the environment) about the rest of 2025. A few months of stock and currency market underperformance vs. the rest of the world does not make a trend. But nor should one ignore these signs. There are clear problems in the US economy and how the economy is being managed. Deficits, debts and tariffs are a shroud over the American economy. Investor money, at least in part, seems to want to invest elsewhere beyond the US. It may well be wise to increase international equity allocations to take advantage of still-discounted valuations outside of America.

A FINAL THOUGHT…

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at https://www.baldwinmgt.com/disclosure/.

Peter H. Havens, Chairman

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.