FUNDAMENTAL vs. EMOTIONAL

In the midst of another war in the Middle East and this time with Iran, it is easy to lose a sense of direction, to become confused with information coming from all sides and most of it contradicting. It is hard not to be swayed by emotions and many people during confusing times will make emotional decisions. So let us first ground ourselves with facts, remind ourselves of what is and then move forward with what might be.

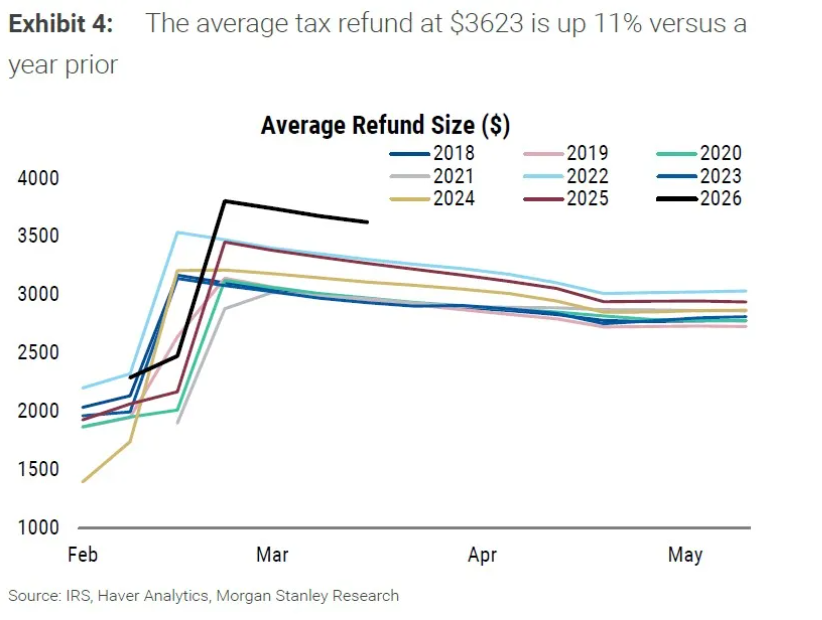

Earnings season for Q4 2025 recently finished for corporate America, and companies generally did better than expected by analysts on Wall Street. Earnings growth was +13.2% year over year and sales growth was +8.6% for the S&P 500 (1). The vast majority of companies (76.5%) exceeded earnings projections and 66.3% of companies beat analysts’ revenue projections (2). Further, corporate net profit margins averaged 13.2%, which again surprised analysts to the upside (3). So overall, 2025 was a fine year for corporate results. Also very importantly, management outlooks for the first quarter of 2026 and for the full year were upbeat and supported Wall Street 2026 estimates of company earnings growth of 14% – 15% and sales growth of 7.2% (4). Notably, even without the so-called “Mag 7” (think Nvidia, Meta, and Alphabet), Wall Street is forecasting that company earnings for the other 493 companies of the S&P 500 will be +12.5% (5). What will be the fundamental support for the rosy outlooks? First, there will be tax refunds from the U.S. government because of the “One Big Beautiful Bill” passed earlier in 2025.

This should allow for greater consumer and corporate spending. There will also be major fixed investments made in the U.S. as a result of trade deals done with various countries (think Japan, Taiwan, Germany, the U.K.) and companies like Taiwan Semiconductor and Samsung. Projections by economists total hundreds of billions of dollars of foreign investments. Even though the tariffs used to “strong arm” the investments were declared illegal by the U.S. Supreme Court; to date no countries or companies have walked back from their deals. Not to be forgotten are the artificial intelligence (AI ) infrastructure buildouts to support the rapid adoption of AI. These also are slated to range in hundreds of billions of dollars, and have been announced by companies like Microsoft, Alphabet, Oracle, Nvidia and Meta. As the AI infrastructure spreads, it is expected that greater corporate use of AI may enhance company productivity, first through lowering costs (thereby enhancing margins), and then by generating more revenue and more sales per employee, further enlarging corporate margins. Greater productivity, especially productivity per employee, should dampen inflation, which should allow the Federal Reserve to lower interest rates in the coming year. Reducing the cost of money will spur economic growth.

BUT………

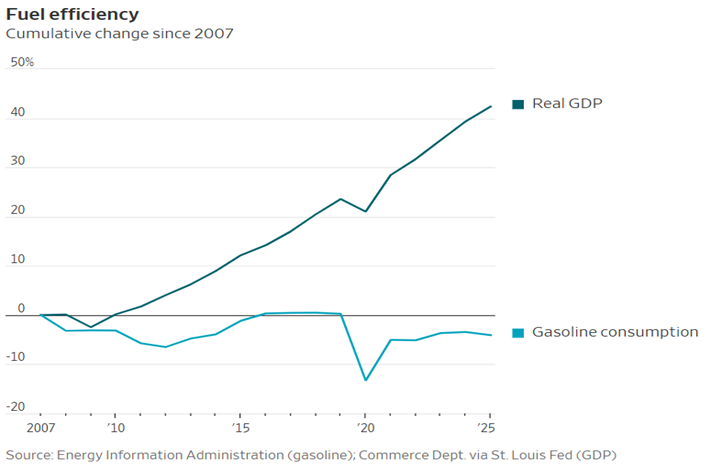

Despite all the aforementioned support for economic and corporate growth in 2026, there is a war in the Middle East and with Iran, no less. As this is being written, the Strait of Hormuz is effectively being blocked by Iranian threats to international shipping. Vessel owners and insurers have idled ships on either side of the Strait, not willing to risk sailing for fear of being attacked. Consequently, the flow of oil, liquid natural gas (LNG), fertilizer and aluminum (to name a few important products) out of the Persian Gulf have stopped, causing prices of those products to rise. This interruption of products is damaging to the world’s economy, and the longer the interruption lasts, the more consequential the ill effects. But let’s add some perspective, especially regarding effects on the American economy. Higher oil prices are like a tax on a consumer. In the past, the American economy was much more energy dependent than it is today. In fact, the U.S. consumed 4% less gasoline in 2025 than it did in 2007, while producing 47% more goods and services, adjusted for inflation.

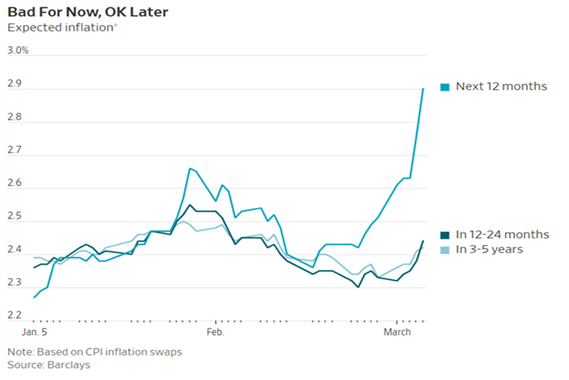

American households’ consumption of energy (including electricity, natural gas and gasoline) fell from 5.7% of GDP in 2007 to 3.7% in 2025. At the same time, the U.S. has become an exporter of petroleum and a major exporter of LNG – all due to improved technology use in American oilfields. So, while American consumers will be hit with higher prices for hydrocarbons, American oil companies will benefit from higher hydrocarbon pricing. Currently, the futures markets do not expect oil pricing to be elevated for long as prices for oil several months out are less than near term prices. Current futures market pricing suggests expectations that the the Strait of Hormuz may reopen in the near term, and the oil will flow again from the Persian Gulf, though there is no certainty. Inflation may get a measurable “bump” because of heightened oil prices – but again the futures markets are currently predicting that inflation will fall a year from now.

Adding to the confusion of a Middle East war are tariffs – which have alienated global trading partners and increased costs for American consumers and have been declared illegal in their present form by the U.S. Supreme Court. The American government is pivoting its tariff strategy by using other methods, which are more cumbersome to use and demand Congressional input, but they are likely to be implemented, nevertheless. So, tariffs and their associated confusion have not gone away.

Lastly, the U.S. employment picture has become a bit murkier. It is not yet dark, but it is not brilliant either. Unemployment is still historically low. Yet employment has slowed. Employees are fearful of AI and its effects on redundancies. Some pundits have proclaimed that millions of jobs will be lost to AI. But the jobs will not disappear all at once and new jobs will certainly be created. Further, productivity will be enhanced and inflation will be dampened.

OVERSEAS………

Internationally, markets year to date are performing better than the U.S., as they did in 2025. But since the start of the war, the U.S. markets have been less volatile than their global counterparts. Fiscal policies overseas are being loosened as defense spending continues to rise with increased tensions around the globe, and foreign markets are still considered cheap compared to the U.S. – but not as inexpensive as they once were. The dollar has rallied since the start of the Iran war in a flight to perceived safety – but it is still down vs. others over the last 15 months. Investment opportunities still exist overseas, but markets are more worried about energy reserves in Europe and Asia vs. America. For example, American April natural gas futures recently traded down 57% from the peak in January during winter storms and about 28% lower than one year ago. In Europe, benchmark gas prices recently traded +67% because inventories are lower than normal after a chilling winter season. Foreign governments are trying to negotiate separate deals with Iran to allow their flagged vessels to pass through the Strait and restart the flow of energy to their countries. The U.S. is also calling on allies to help it reopen the Gulf by joining a task force to escort tankers through the Strait. The U.S. is even thinking of offering insurance cover in addition to the naval escorts to convince ship owners and sailors that the Strait is open for business. There are a lot of people focused on this issue and currently the markets think that it will get solved in the relative near term. Again, for perspective, after the first Gulf War with Iraq, when Saddam Hussein set the Kuwaiti oilfields ablaze as his army was pushed out of Kuwait, experts thought the oilfields of the second largest oil producer in OPEC were too damaged and would be lost to the world.

Months later, the fires were extinguished, the damaged wells were repaired, and Kuwaiti production was brought back online, returning to its pre-war production levels. What was thought impossible to solve was solved – and we believe this current situation in the Gulf will be too – because too many people have a vested interest in getting the Strait opened for business. Further, the U.S. and the world were far more dependent on oil as an energy source in 1991 than today and in the case of America, oil imports from the Persian Gulf are less than 10% of total supplies.

CONCLUDING REMARKS…….

We are not suggesting for an instant that the Iranian War is not a profoundly serious matter, nor that it should be readily overlooked to see a brighter day in the future. We are suggesting that an investor should balance the gloom of the Iranian conflict with the strength of the world’s economy, the rapid advance of a major technology called AI and what it is doing already for productivity, and the fact that the world is no longer as dependent on oil as an energy source as it once was. Throughout an investor’s portfolio, companies with very adept management teams are already thinking of ways to adapt to the situation in Iran. Successful management teams have handled severe challenges in the past and will do so going forward. Superior management protects a company’s assets for its owners in whatever circumstances may arise. Superior managements position those assets to produce increased sales, earnings, cash flows and dividends – and these metrics have historically been associated with stock price performance. Successful investors, in our experience, do not make investment decisions emotionally, reacting to headlines. Rather they base their decision making on long term fundamentals and over a long history. At least in the United States, the stock market has appreciated mightily. We believe that the investment future is no less bright than it has been.

A FINAL THOUGHT ABOUT AFFORDABILITY FROM 2018……

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. Markets remain subject to volatility, geopolitical risks, and unforeseen economic developments. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. Charts used are for illustrative purposes only and are based on historical data and estimates that may not be indicative of future results.

Peter H. Havens, Chairman

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.